Malaysia lies just above the equator, right in the heart of South-East Asia. Strategically located between the Indian Ocean and the South China Sea, Malaysia is well serviced by all primary air and shipping lines. Malaysia’s strong and sustainable economic foundation, its business-ready environment, forward-looking focus, and dynamic workforce have made it an attractive, cost-competitive investment location in the region. It is quickly becoming a preferred centre for shared services and leading technology industries.

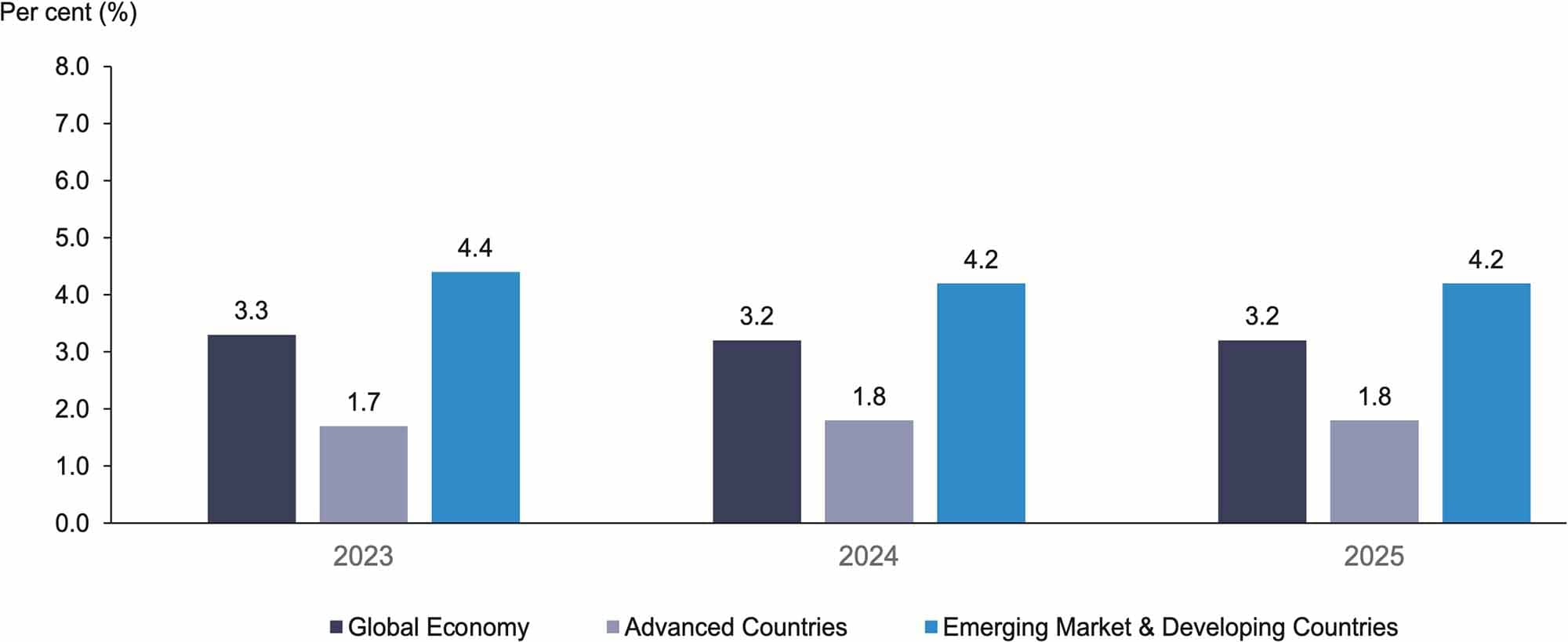

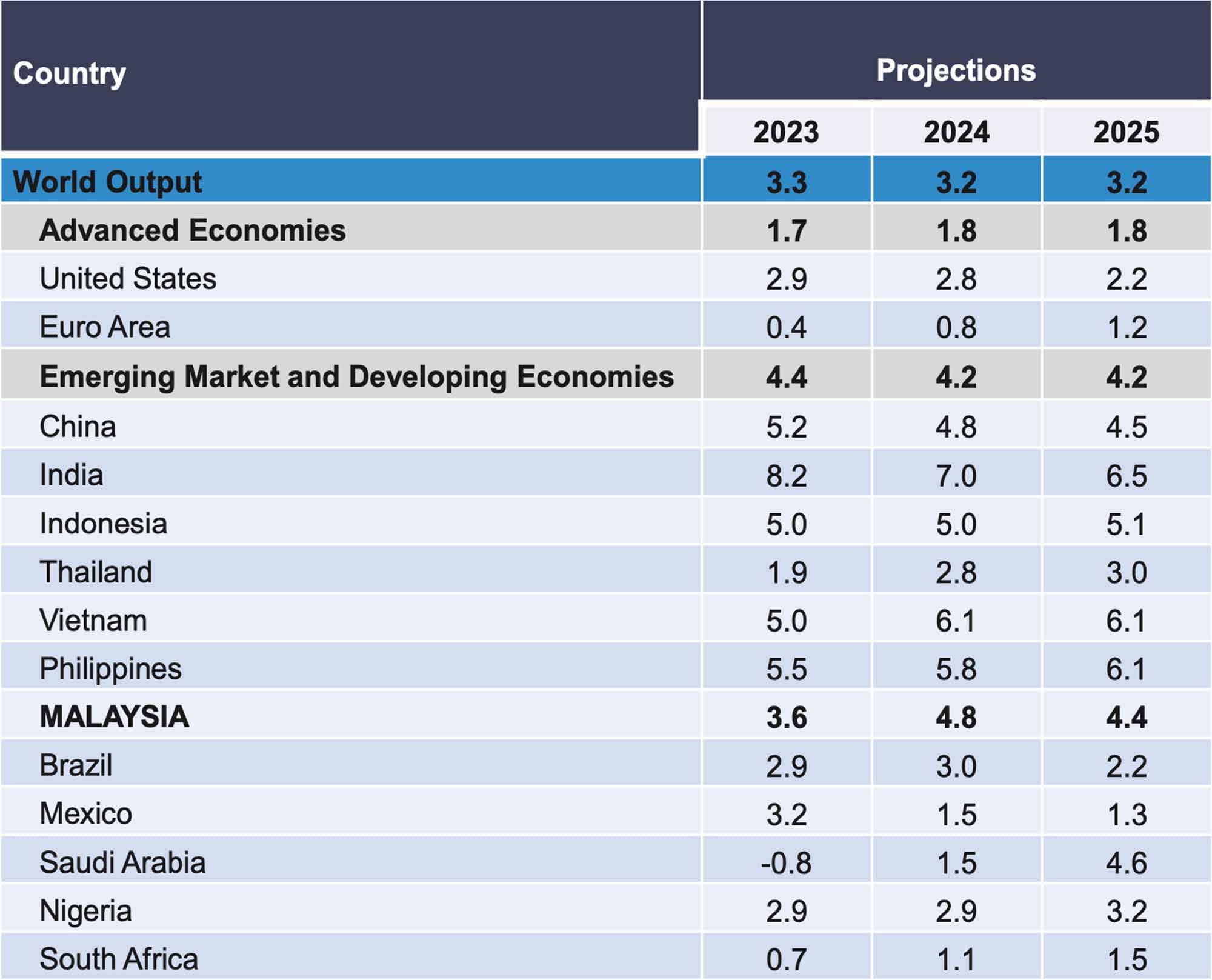

According to the IMF World Economic Outlook (WEO) report for October 2024, global growth is expected to remain stable, with growth projections for 2024 and 2025 remaining at 3.2 per cent, indicating only slight changes from the updated forecasts in the July 2024.

As shown in Chart 1, advanced economies forecast for the year 2024 has been raised to 1.8 per cent, reflecting a more optimistic outlook for economic recovery and stabilisation. The growth forecast for 2025 remains unchanged at 1.8 per cent, indicating a stable outlook for medium-term growth with moderate but consistent expansion.

In emerging markets and developing economies, disruptions in commodity production and delivery due to oil-related conflicts, social unrest and extreme weather events have led to downward revisions in growth projections for the Middle East, Central Asia and Sub-Saharan Africa. However, strong demand for semiconductors and electronics, driven by substantial investments in artificial intelligence, has supported growth in these regions.

The National Bureau of Statistics of China reported that in the first three quarters of 2024, China's GDP reached 94,974.6 billion yuan, recording a 4.8 per cent year-on-year growth at constant prices. By sector, there was growth in the primary industry, which increased by 3.4 per cent (5,773.3 billion yuan) followed by secondary industry which grew at 5.4 per cent (36,136.2 billion yuan) and the tertiary industry with a growth of 4.7 per cent (53,065.1 billion yuan). In terms of quarterly performance, GDP growth in the first quarter was 5.3 per cent, followed by 4.7 per cent in the second quarter and 4.6 per cent in the third quarter.

In the third quarter of 2024, Vietnam's GDP grew at 7.4 per cent year-on-year, fuelled by a 9.1 per cent increased in the industrial and construction sectors especially manufacturing sector which grew at the fastest pace of 11.4 per cent. The services sector rose by 7.5 per cent and agriculture grew at 2.0 per cent. For the first nine months of 2024, GDP increased by 6.8 per cent, with agriculture rose by 3.2 per cent, industry and construction by 8.0 per cent and services by 7.0 per cent. The economic structure for the first nine months showed that agriculture at 11.64 per cent, industry at 37.10 per cent, and services at 42.80 per cent. In terms of expenditure, final consumption grew at 6.2 per cent, contributing 62.7 per cent to overall growth, while exports increased by 17.0 per cent, imports by 17.1 per cent, and the trade balance by 0.7 per cent.

In the third quarter of 2024, Vietnam’s GDP grew by 7.40 per cent year-on-year, fuelled by a 9.11 per cent increase in the industrial and construction sector, with manufacturing leading the growth at 11.41 per cent. The services sector rose by 7.51 per cent, while agriculture grew by 2.58 per cent. For the first nine months of 2024, GDP increased by 6.82 per cent, with agriculture rose by 3.20 per cent, industry and construction by 8.19 per cent and services by 6.95 per cent. The economic structure for the first nine months showed agriculture at 11.64 per cent, industry at 37.10 per cent, and services at 42.80 per cent. In terms of expenditure, final consumption grew by 6.18 per cent, contributing 62.66 per cent to overall growth, while exports increased by 16.94 per cent, imports by 17.05 per cent, and the trade balance by 0.66 per cent.

The Philippine GDP grew by 5.2 per cent year-on-year in the third quarter of 2024. The main drivers of this growth were wholesale and retail trade (5.2%), financial and insurance services (8.8%) and construction (9.0%). Among the major sectors, industry and services expanded by 5.0 per cent and 6.3 per cent, respectively, while the agriculture, forestry and fishing sector saw a decline of 2.8 per cent. On the demand side, household consumption was the largest contributor, rose by 5.1 per cent. Government spending grew by 5.0 per cent, gross capital formation (13.1%) and imports of goods and services (6.4%). However, exports of goods and services dropped by 1.0 per cent.

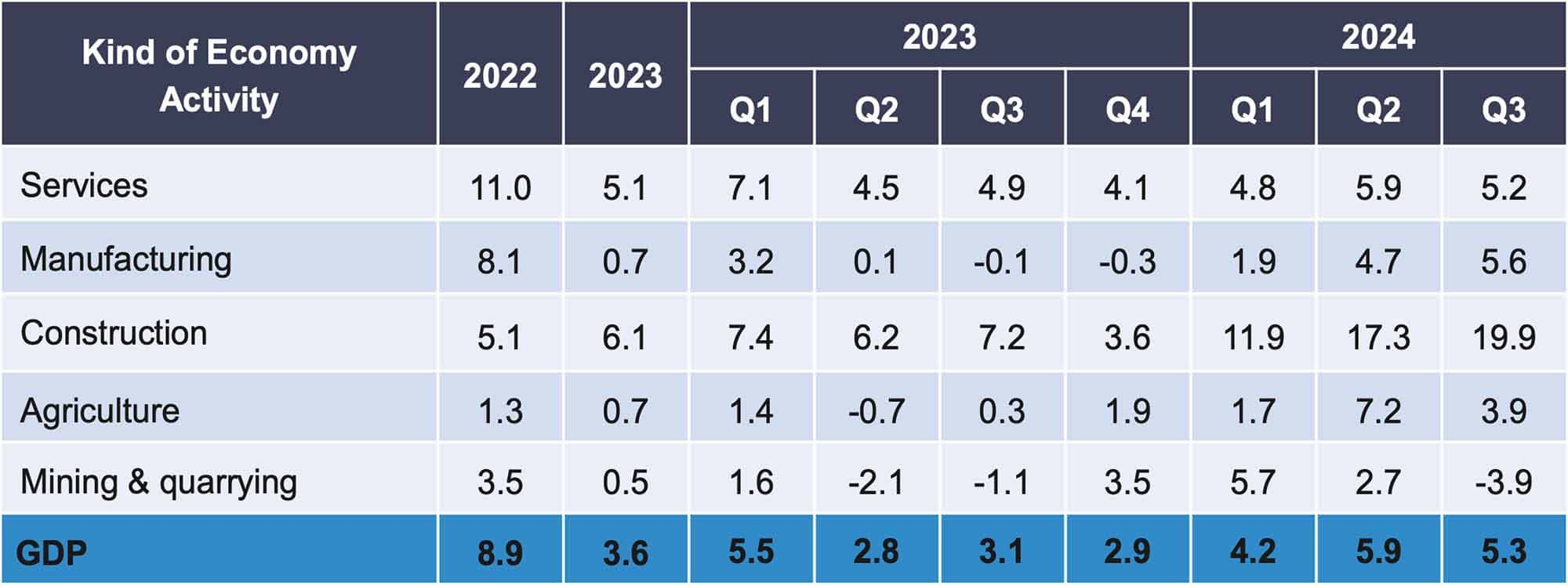

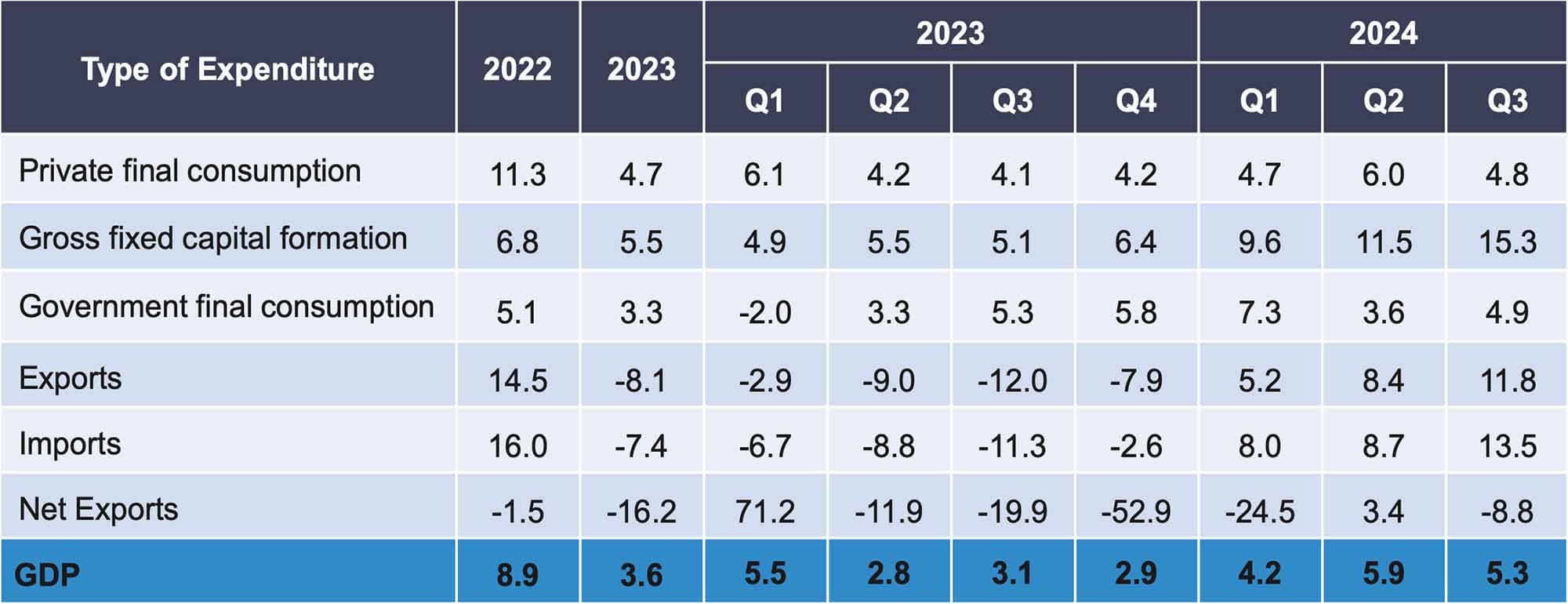

Malaysia’s economy expanded by 5.3 per cent in the third quarter of 2024, from the 5.9 per cent growth recorded in the previous quarter (Table 2). The performance on the supply side was mainly supported by the Services, Manufacturing and Construction sectors. Meanwhile, on the demand side, Private final consumption expenditure continued to be the main driver, followed by expenditure in Gross fixed capital formation.

The Services sector recorded a growth of 5.2 per cent from 5.9 per cent in the last quarter. The performance of the Services sector was led by the Wholesale and retail trade sub-sector, which increased 4.2 per cent (Q2 2024: 4.8%). Likewise, the Transportation and storage sub-sector maintained double-digit growth of 10.6 per cent (Q2 2024: 10.5%), while the Business services sub-sector increased 8.5 per cent (Q2 2024: 8.4%).

The Manufacturing sector has showed a better growth in this quarter, increased by 5.6 per cent, as compared to 4.7 per cent in the second quarter of 2024. The growth was driven by all sub-sectors, especially the Electrical, electronic and optical products, which increased by 5.6 per cent (Q2 2024: 3.0%) and Petroleum, chemical, rubber and plastic products, which rose by 4.4 per cent (Q2 2024: 4.1%). Additionally, Non-metallic mineral products, basic metal & fabricated metal products and Vegetable and animal oils & fats and food processing products continued to grow in this quarter, with an increase of 9.2 per cent and 7.6 per cent, respectively.

The Construction sector maintained its strong performance in the third quarter of 2024, with a growth of 19.9 per cent, up from 17.3 per cent recorded in the previous quarter. The strong growth was underpinned by robust performance across all segments, particularly the Non-residential buildings, which accelerated to impressive double-digit growth of 28.1 per cent (Q2 2024: 2.8%) and Specialised construction activities, which grew at 21.7 per cent (Q2 2024: 27.0%). Furthermore, Residential buildings and Civil engineering also showed double-digit growth of 22.7 per cent (Q2 2024: 14.1%) and 10.7 per cent (Q2 2024: 23.6%), respectively.

The Agriculture sector recorded slower growth of 3.9 per cent as compared to the 7.3 per cent in the second quarter of 2024. The performance was largely due to the Oil palm sub-sector which grew at 7.3 per cent (Q2 2024: 19.0%) resulted from a slower production of fresh fruit bunches. Besides, the Other agriculture sub-sector increased by 1.8 per cent (Q2 2024: 0.6%) and Livestock sub-sector rose to 2.7 per cent (Q2 2024: 5.8%).

The Mining and quarrying sector contracted by 3.9 per cent in this quarter, from a growth of 2.7 per cent in the second quarter of 2024. The downturn was mainly influenced by decline in the production of Crude oil & condensate and Natural gas, with decreased of 7.3 per cent (Q2 2024: 1.6%) and 2.8 per cent (Q2 2024: 2.9%), respectively. However, Other mining & quarrying and supporting services posted a modest growth of 2.6 per cent (Q2 2024: 7.2%).

Shifting towards the demand side of the economy, Private final consumption expenditure increased by 4.8 per cent (Q2 2024: 6.0%), driven by the consumption of Transport, Restaurants & hotels and Food & non-alcoholic beverages.

In addition, Gross fixed capital formation (GFCF) accelerated to 15.3 per cent in this quarter from 11.5 per cent in the preceding quarter. The performance of GFCF was backed by the significant growth in the Structure and Machinery & equipment at 18.6 per cent (Q2 2024: 12.6%) and 12.3 per cent (Q2 2024: 11.8 %), respectively. Additionally, Other assets expanded 10.7 per cent as compared to 4.2 per cent in the preceding quarter. In terms of GFCF by sector, the Private sector, which accounted for 80.0 per cent of GFCF, grew at 15.5 per cent (Q2 2024: 12.0%). Moreover, GFCF in the Public sector expanded by 14.4 per cent from 9.1 per cent in the previous quarter.

Government final consumption expenditure expanded to 4.9 per cent from 3.6 per cent in the previous quarter, led by spending on supplies and services. Meanwhile, Imports accelerated higher than Exports to in this quarter with the growth of 13.5 per cent (Q2 2024: 8.7%) and 11.8 per cent (Q2 2024: 8.4%), respectively. Thus, Net exports contracted by 8.8 per cent as compared to an increase of 3.4 per cent in the preceding quarter.

In the third quarter of 2024, Malaysia’s Current Account Balance (CAB) registered a surplus of RM2.2 billion, primarily bolstered by net exports of goods and a lower deficit in Services. Conversely, the Financial Account recorded a net outflow of RM7.5 billion, a shift from a net inflow of RM17.1 billion in the previous quarter. Foreign Direct Investment (FDI) reported a higher net inflow of RM14.5 billion, up from RM9.1 billion in the preceding quarter. Meanwhile, Direct Investment Abroad (DIA) showed an increased net outflow of RM18.9 billion as compared to RM5.3 billion in the previous quarter.

Malaysia’s trade in October 2024 showed steady growth, where the total trade increased by 2.1 per cent or RM4.9 billion, reaching RM244.3 billion from RM239.3 billion in the same month of the preceding year. Exports rose by 1.6 per cent or RM2.0 billion to RM128.1 billion, while imports increased by 2.6 per cent or RM3.0 billion to RM116.1 billion compared to RM113.2 billion the prior year. Additionally, the trade balance continued to show a surplus of RM12.0 billion or 7.6 per cent decreased from RM13.0 billion in October 2023. As compared to September 2024, exports, imports and total trade grew at 3.7 per cent, 4.8 per cent and 4.2 per cent, respectively. Conversely, the trade surplus declined by 6.2 per cent or RM0.8 billion, from RM12.8 billion.

The labour force continued to expand in the third quarter of 2024, with an increase of 0.7 per cent or 114.4 thousand persons, reaching a total of 17.26 million persons (Q2 2024: 17.15 million persons). Subsequently, the labour force participation rate (LFPR) remained at 70.5 per cent in the third quarter of 2024. As for the year-on-year comparison, the labour force registered an increase of 2.6 per cent to 17.26 thousand persons (Q3 2023: 16.82 million persons), while the LFPR went up by 0.4 percentage points to 70.5 per cent (Q3 2023: 70.1%).

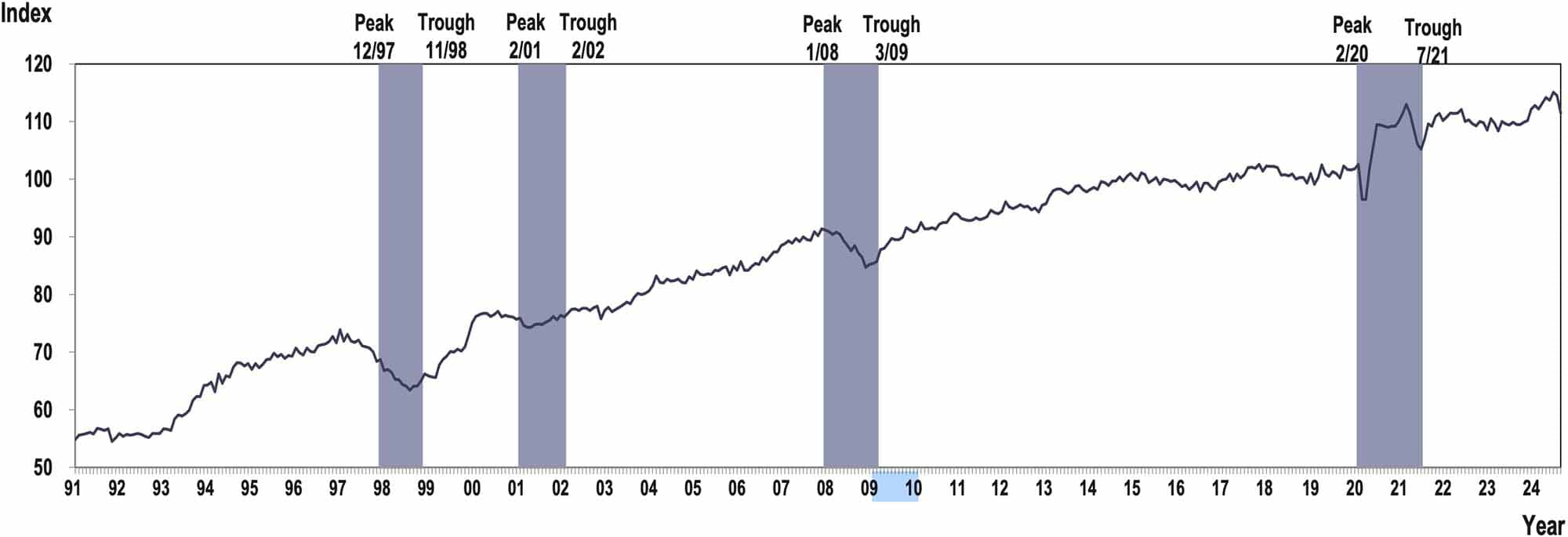

In September 2024, the annual growth of Malaysia’s Leading Index (LI) remained positive by recording 1.8 per cent, reaching 111.5 points as compared to 109.5 points in the same month of the previous year. The Bursa Malaysia Industrial Index was the main contributor to this increase, rising by 30.4 per cent. However, the monthly performance of the LI declined by 2.6 per cent due to decreases in most components, except for the Real Money Supply, M1 and Bursa Malaysia Industrial Index, accounting for 0.2 per cent respectively. Looking at the smoothed long-term trend in September 2024, the LI consistently exceeded 100.0 points, indicating that the Malaysian economy is expected to continue growing, backed by optimistic domestic economic performance. Nonetheless, global challenges may pose potential risks to this growth trajectory.

Besides, Businesses expect an optimistic economic surrounding the fourth quarter of 2024, with a positive confidence indicator of +4.8 per cent, the highest since the second quarter of 2022. Looking ahead, business prospects for the period October 2024 to March 2025 remain favourable, with a net balance of +13.8 per cent as against +23.5 per cent previously recorded. All sectors predict improved business prospects during the next six months. Sentiment in the Services sector is positive, with a net balance of +27.5 per cent for the same period, compared to +30.8 per cent in the previous quarter. The Wholesale and Retail Trade sector likewise expects a positive business outlook, with a net balance of +16.7 per cent from +10.6 per cent recorded previously. Concurrently, the Construction sector foresees a favourable business environment, with a net balance of +16.0 per cent compared to +21.7 per cent earlier. The Industry sector anticipates an improved business outlook, with a net balance of +4.3 per cent for the period of October 2024 to March 2025.

National Real Estate Award Firm of the Year 2021, 2022, 2023, 2024

National Real Estate Award Industrial Firm of the Year 2020, 2022, 2023

National Real Estate Award Technology Firm of the Year 2021

National Real Estate Award Real Estate Agent of the Year 2020

National Real Estate Award Specialised Project of the Year 2019

National Real Estate Award CEO

National Real Estate Award Commercial Agency

National Real Estate Award Million Dollar Roof Top

National Real Estate Award Top Realtor

Star Property Best Practice Award 2019

Star Property All-Star Agency 2017

iProperty Elite Project Marketing Agency

iProperty Agency of the Year (Platinum)

Asia Pacific Property Awards

Asia Pacific Residential Property Awards