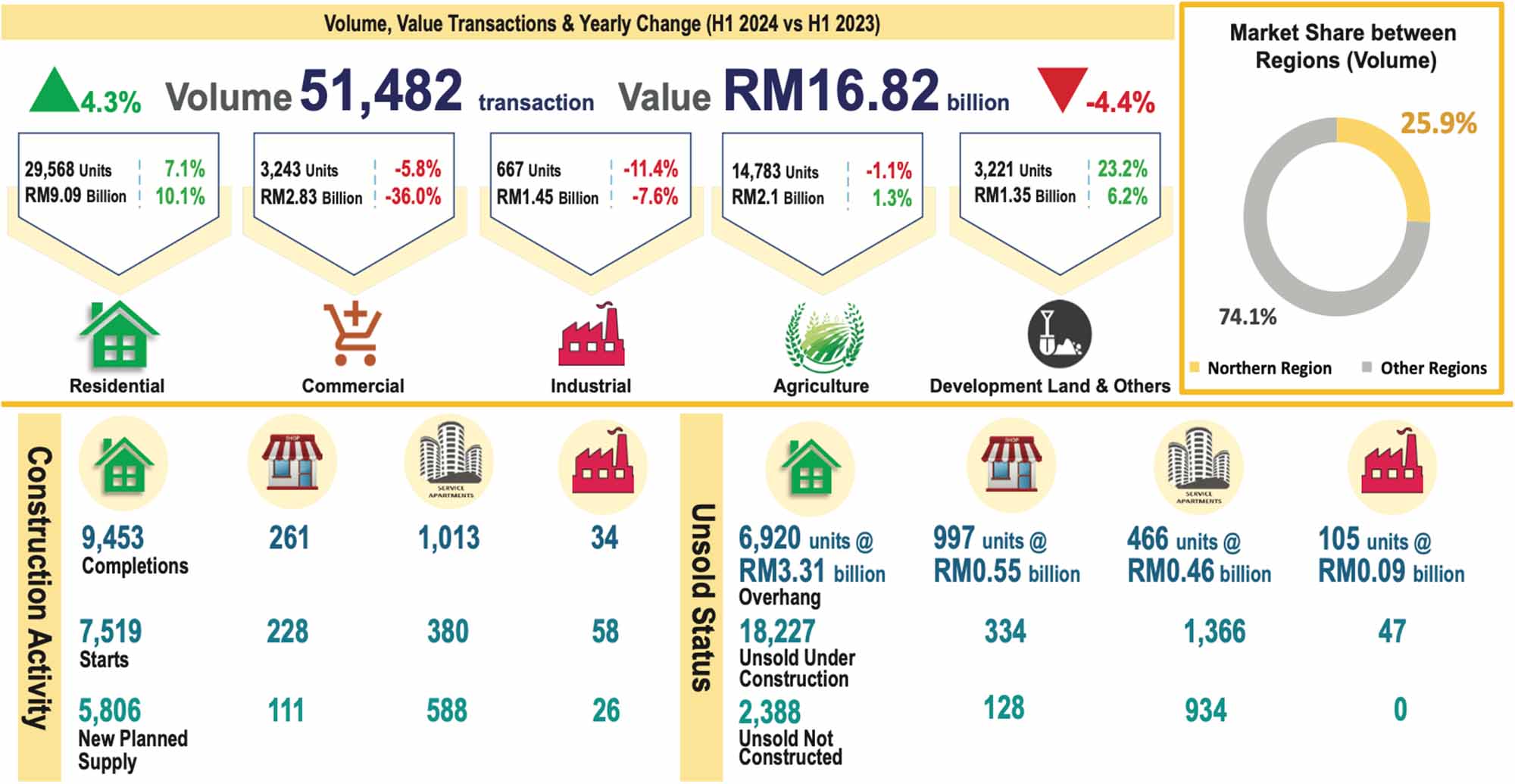

The performance of the Northern Region property market was moderate in H1 2024. The volume and value of transactions showed a mixed performance compared to H1 2024. The region registered 51,482 transactions worth RM16.8 billion, showing a 4.3% increase in volume compared to H1 2023 but value decreased by 4.4%. Combined, these four states within the region formed 25.9% and 15.9% of the national volume and value transactions, respectively.

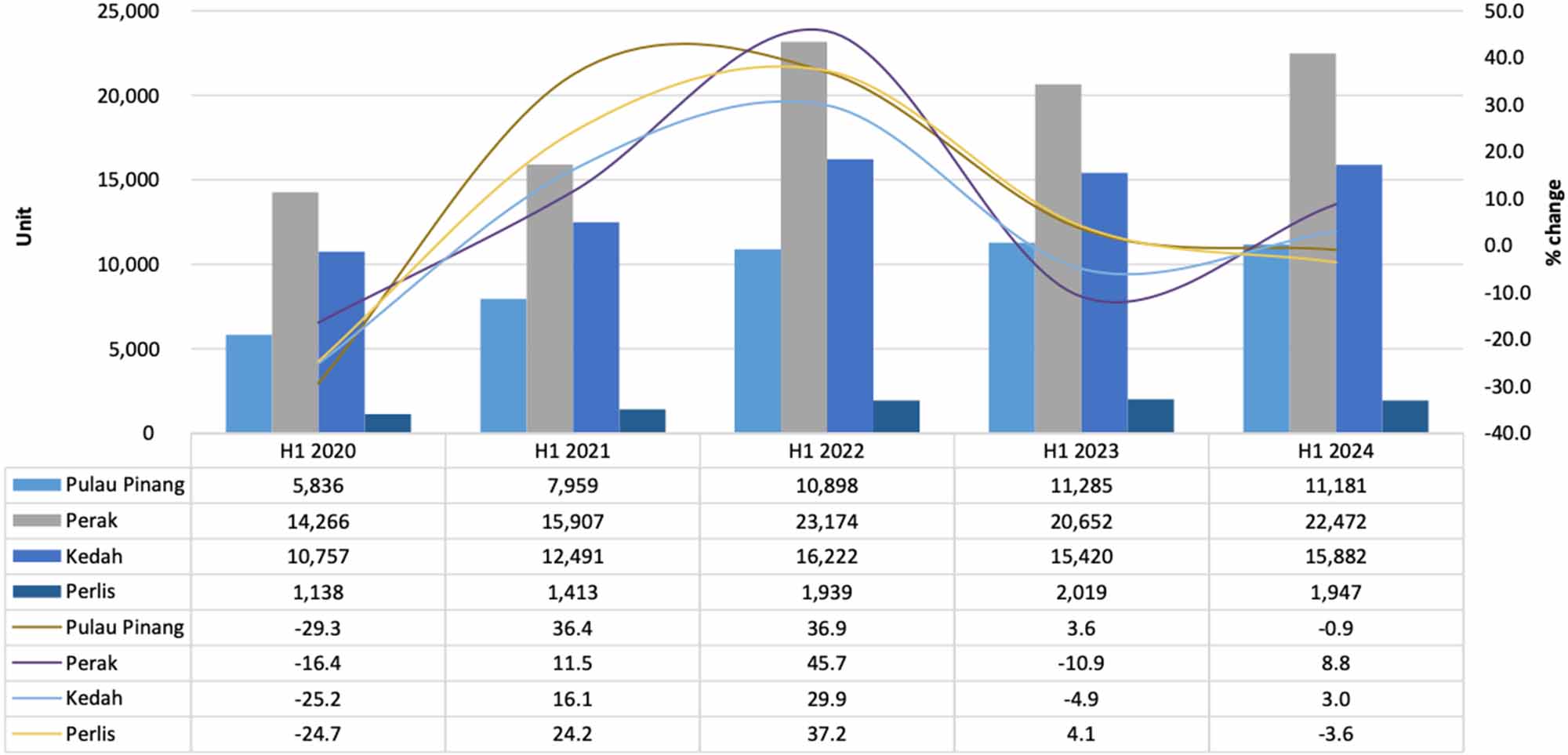

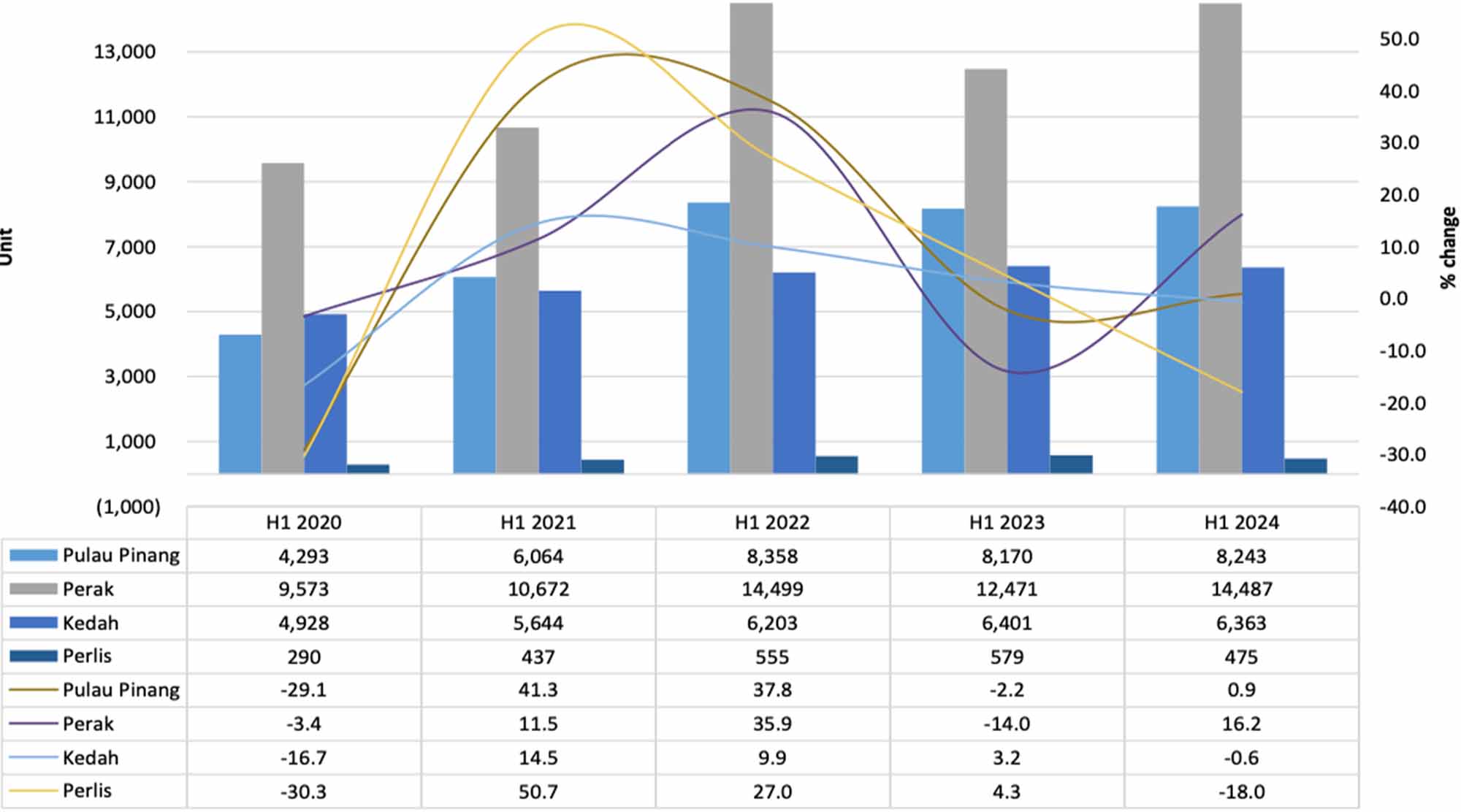

The property market activity for Perak and Kedah, showed an upward trend in the review period, increased (8.8%) and 3.0%, respectively. Meanwhile another two states showed the opposite trend, contracted 3.6% in Perlis and 0.9% in Pulau Pinang.

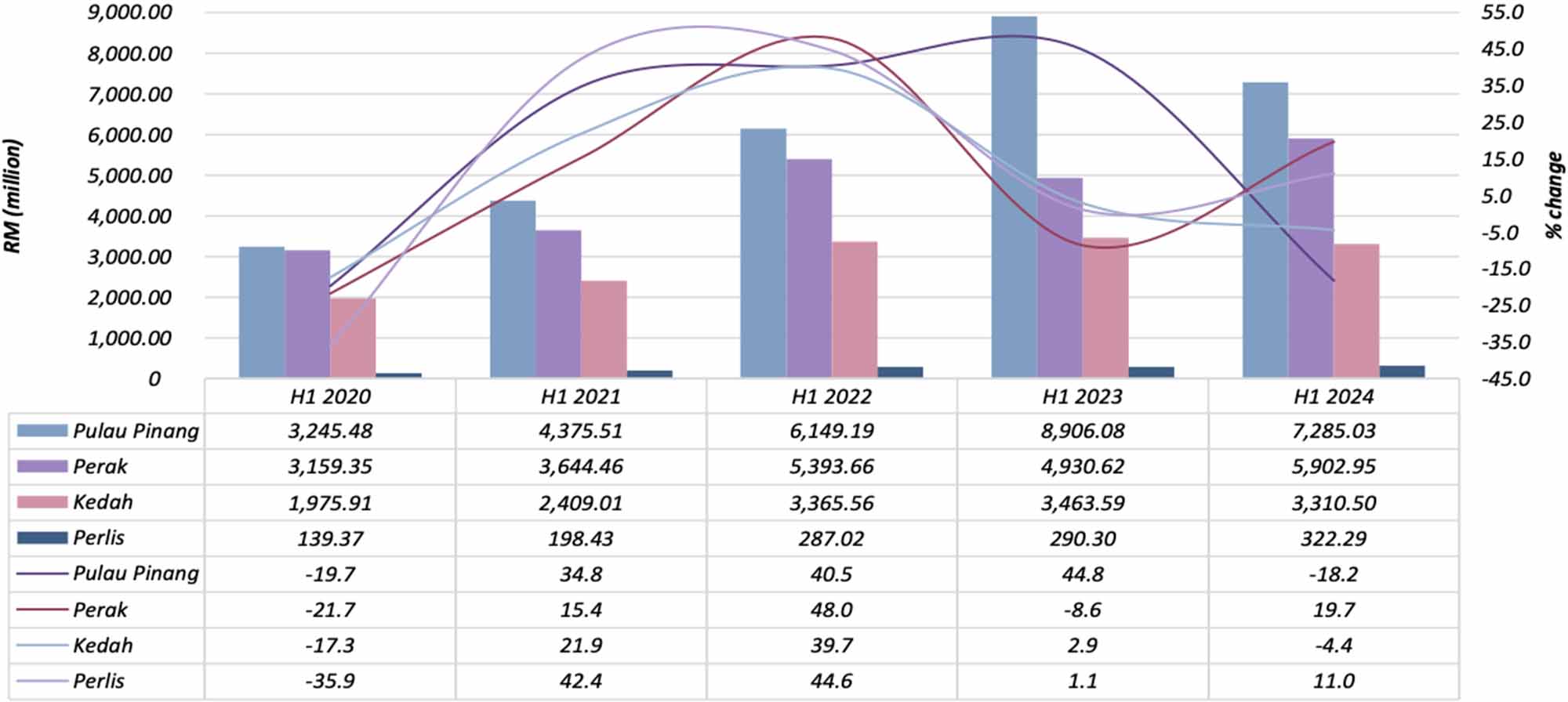

Transaction values showed similar a mixed movementin the review period. Perak increased by 19.7%and followed by Perlis (11.0%), while Pulau Pinangand Kedah experienced a drop of 18.2% and 4.4%,respectively.

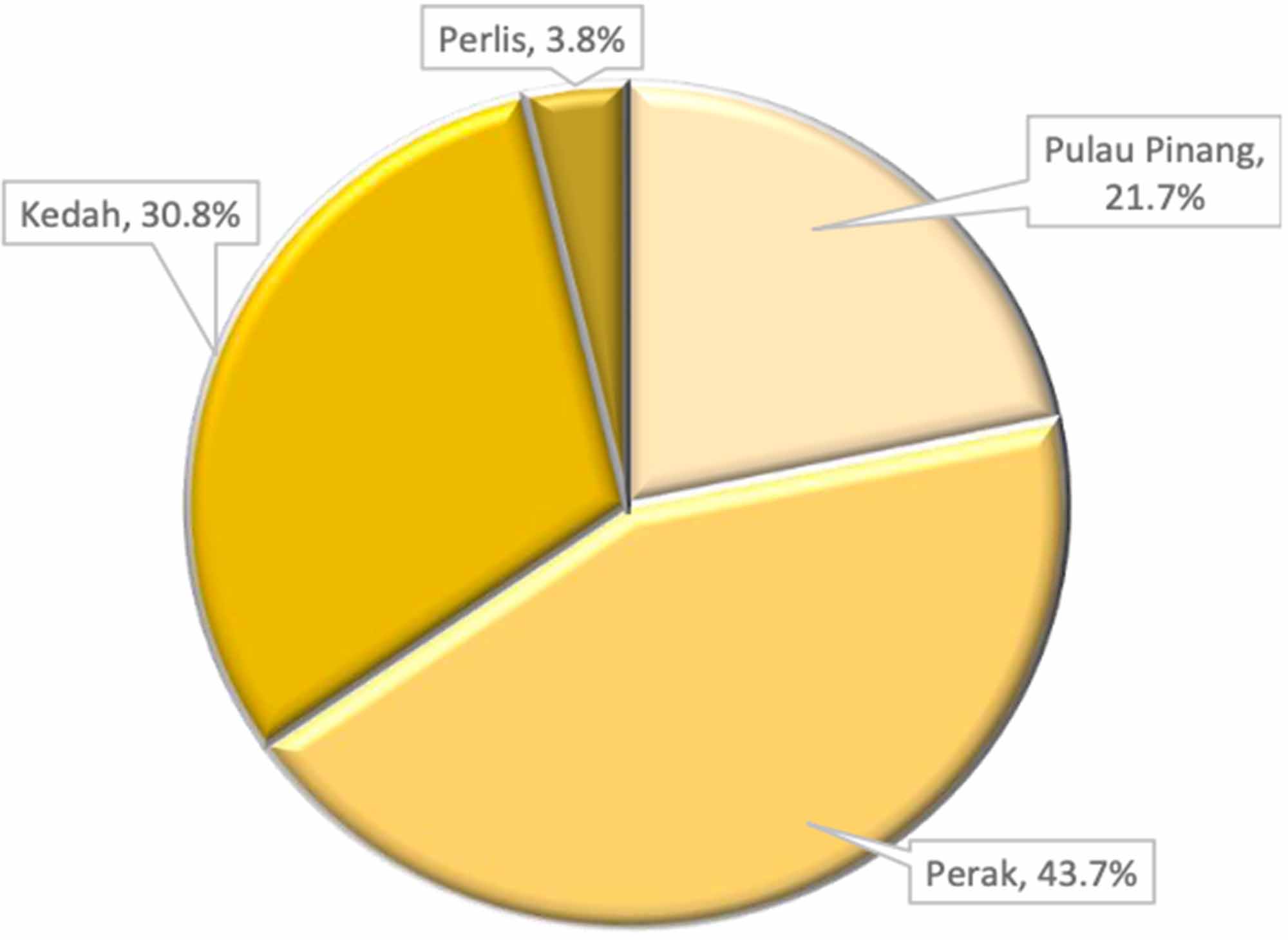

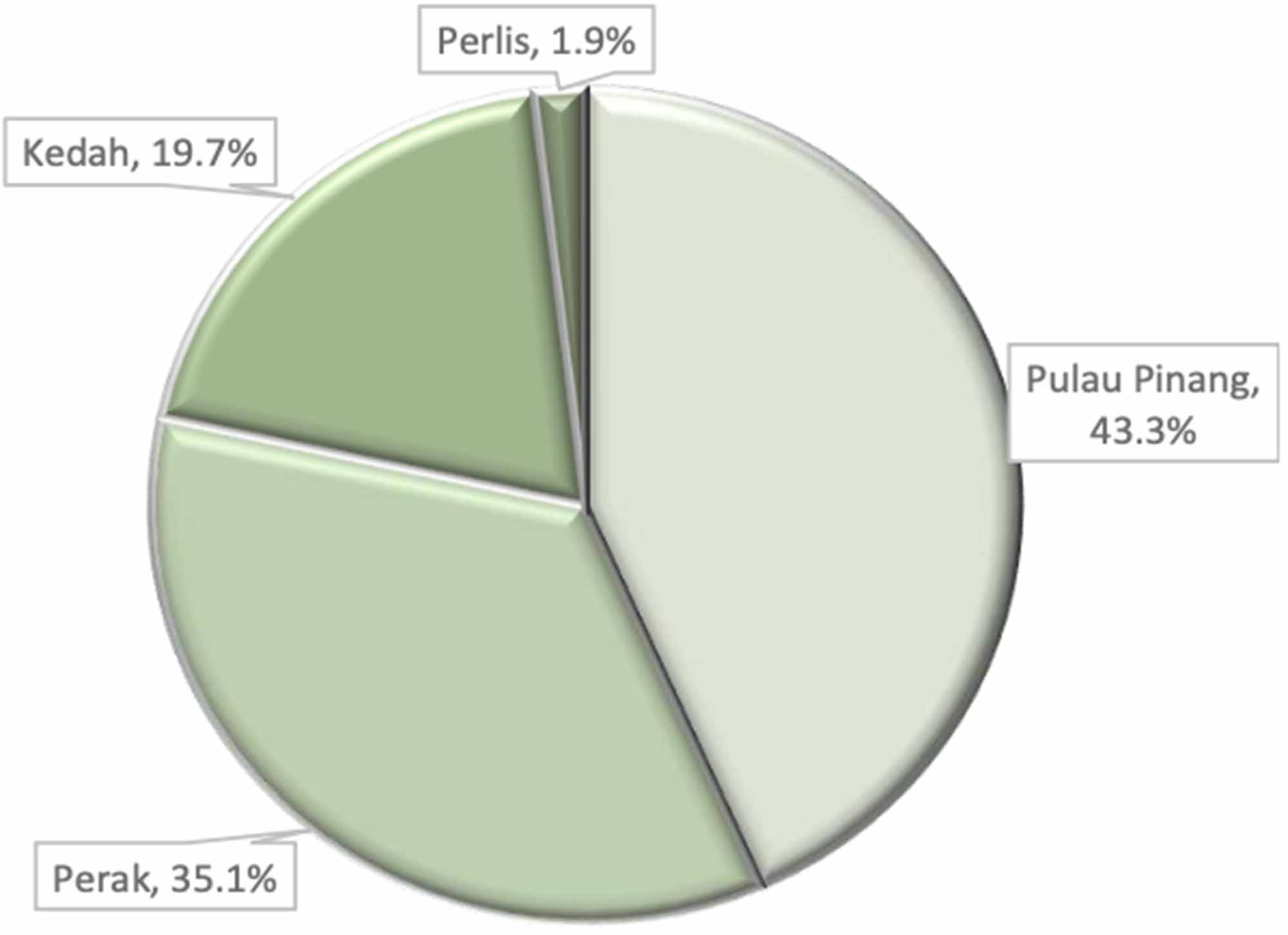

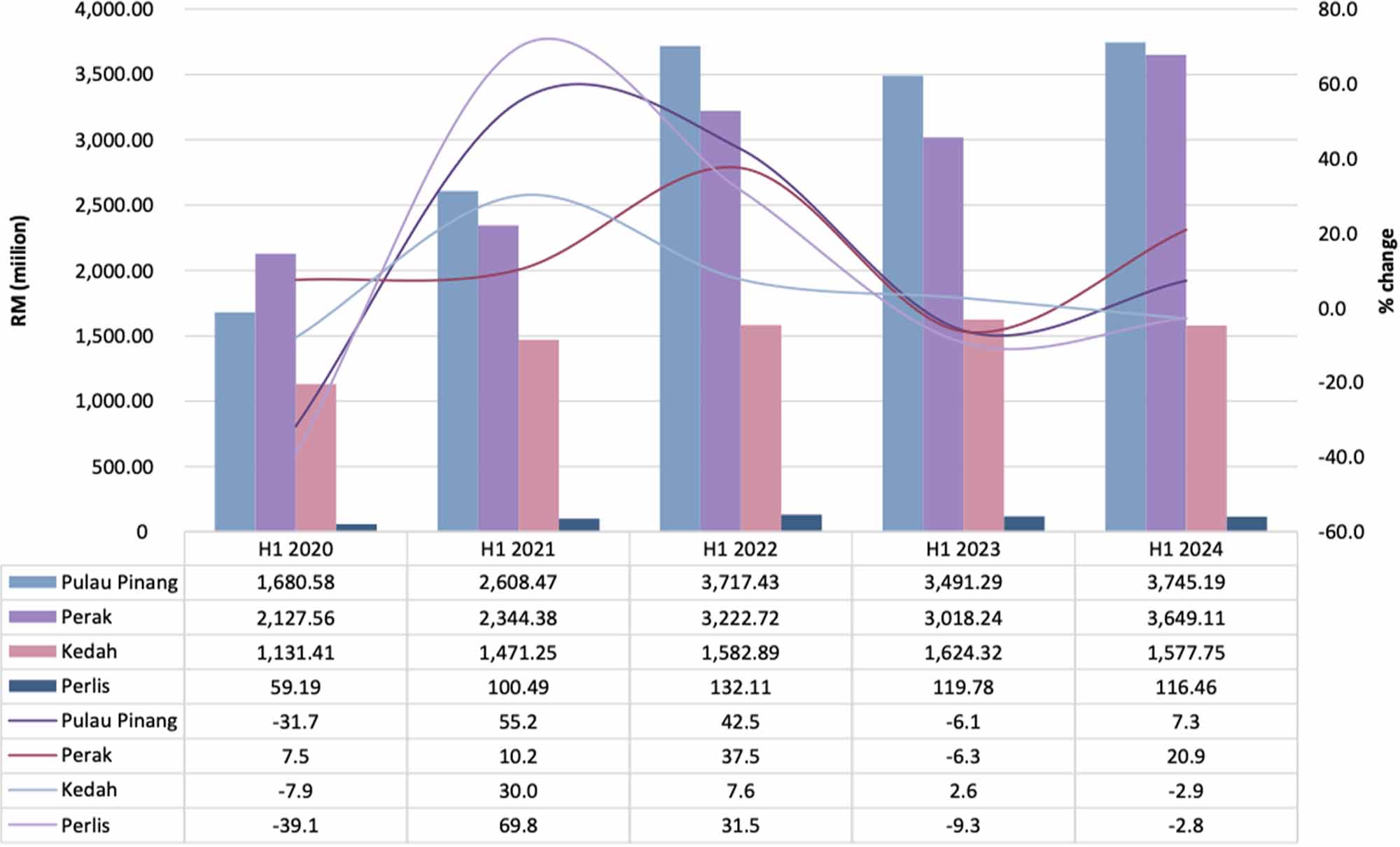

By state, Perak recorded the highest volume of transactions (22,472 transactions), which contributed 43.7% of the Northern Region total transactions. However, in terms of transaction value, Pulau Pinang led the region with 43.3% (RM7.29 billion) of the total.

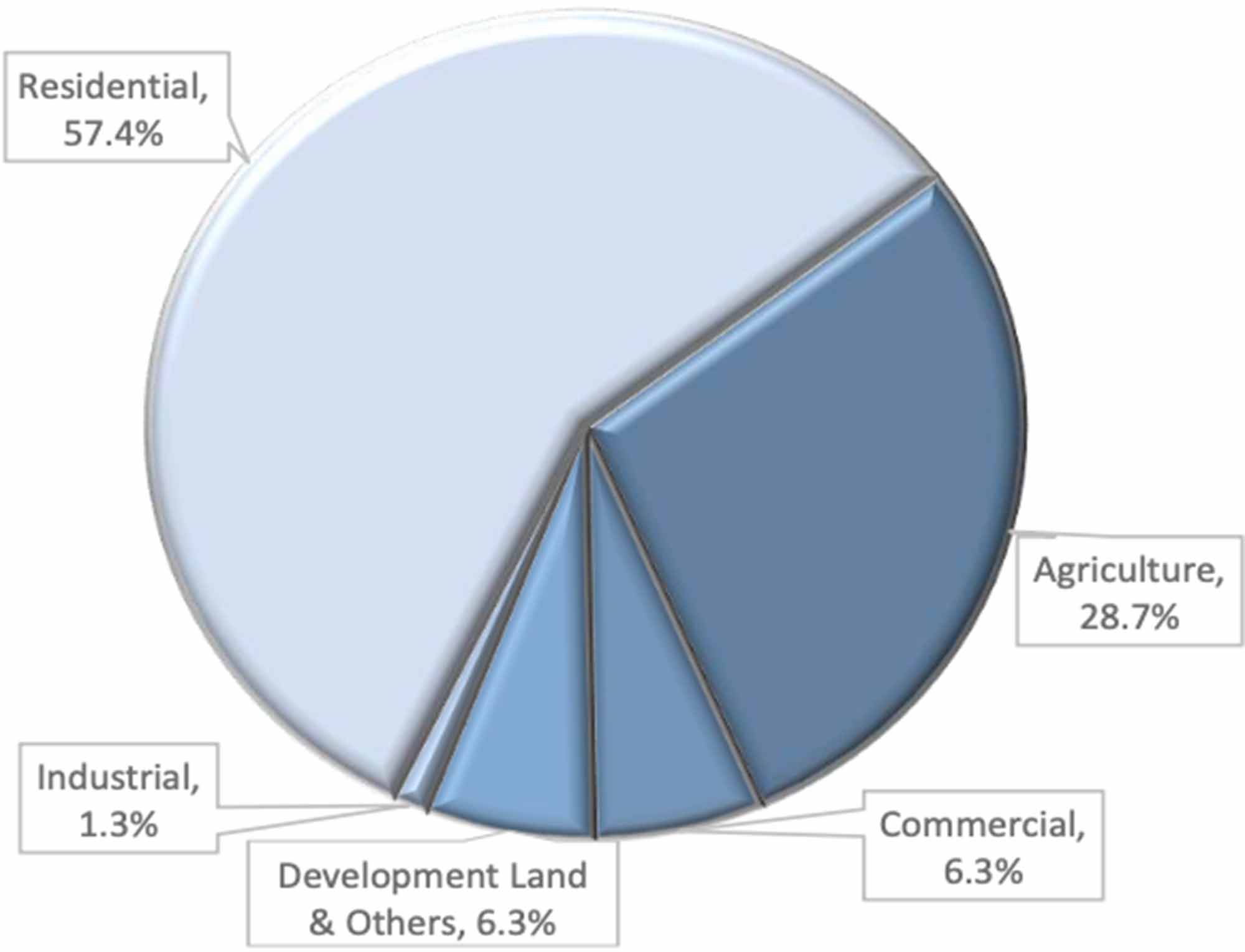

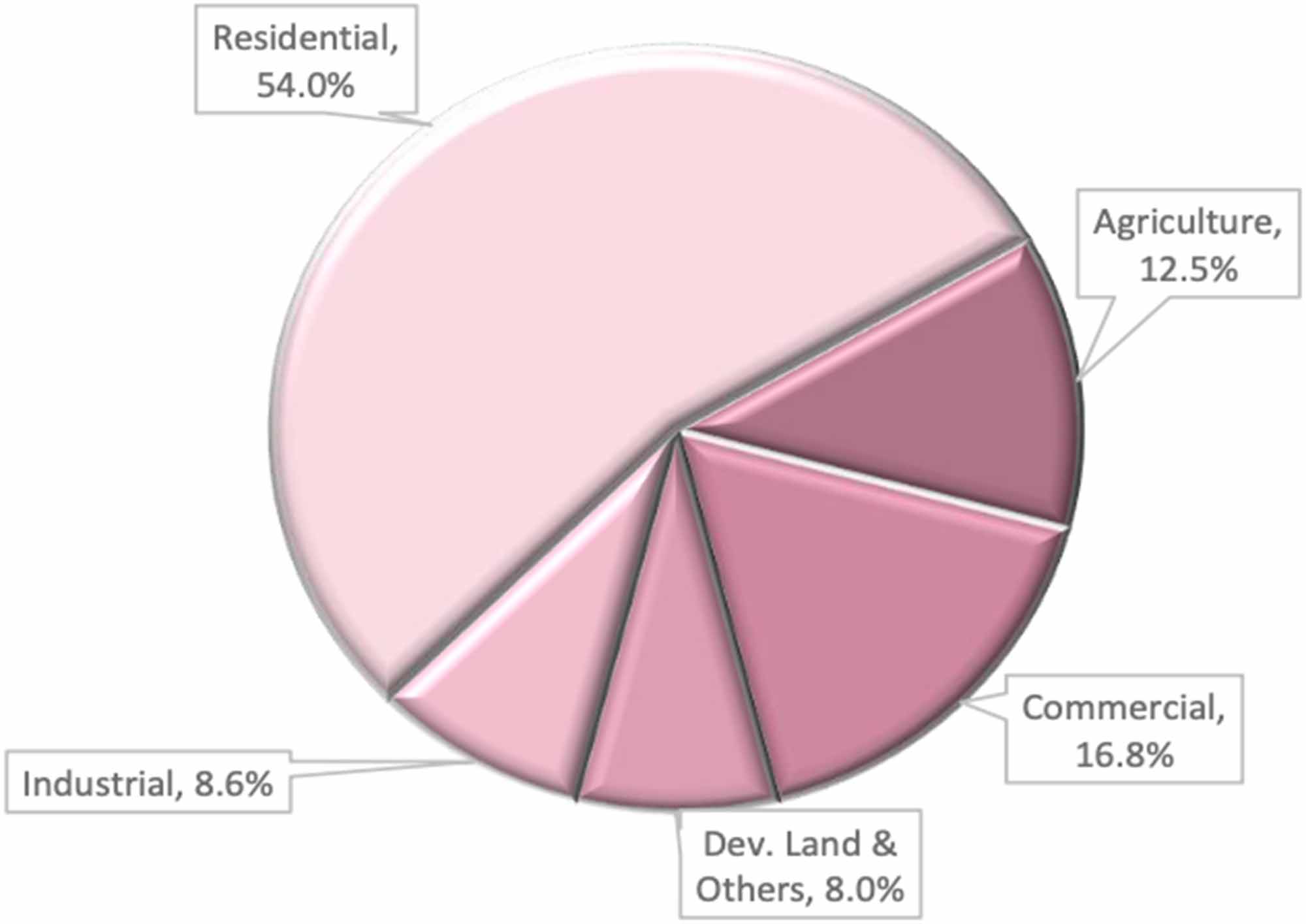

For the Northern Region, residential property continued to be the most actively transacted sub-sector, representing 57.4% (29,568 transactions) of the total transactions. The main contributors to residential transactions were Perak, Pulau Pinang and Kedah. Likewise, the residential sub-sector dominated the region’s overall property transaction value with 54.0%.

The transaction volume for residential sub-sector improved for Perak and Pulau Pinang, which increased by 16.2% and 0.9%, while Perlis and Kedah experienced the opposite, dropped by 18.0% and 0.6%, respectively.

In terms of transaction value, Perak showed an increase of 20.9%, followed by Pulau Pinang by 7.3%. Contrarily, another two states showed a downward trend, led by Kedah (2.9%), and Perlis (2.8%).

In terms of transaction value, Kuala Lumpur and Selangor recorded an increase of 14.3% and 10.3%, respectively, whereas Putrajaya decreased by 43.0%.

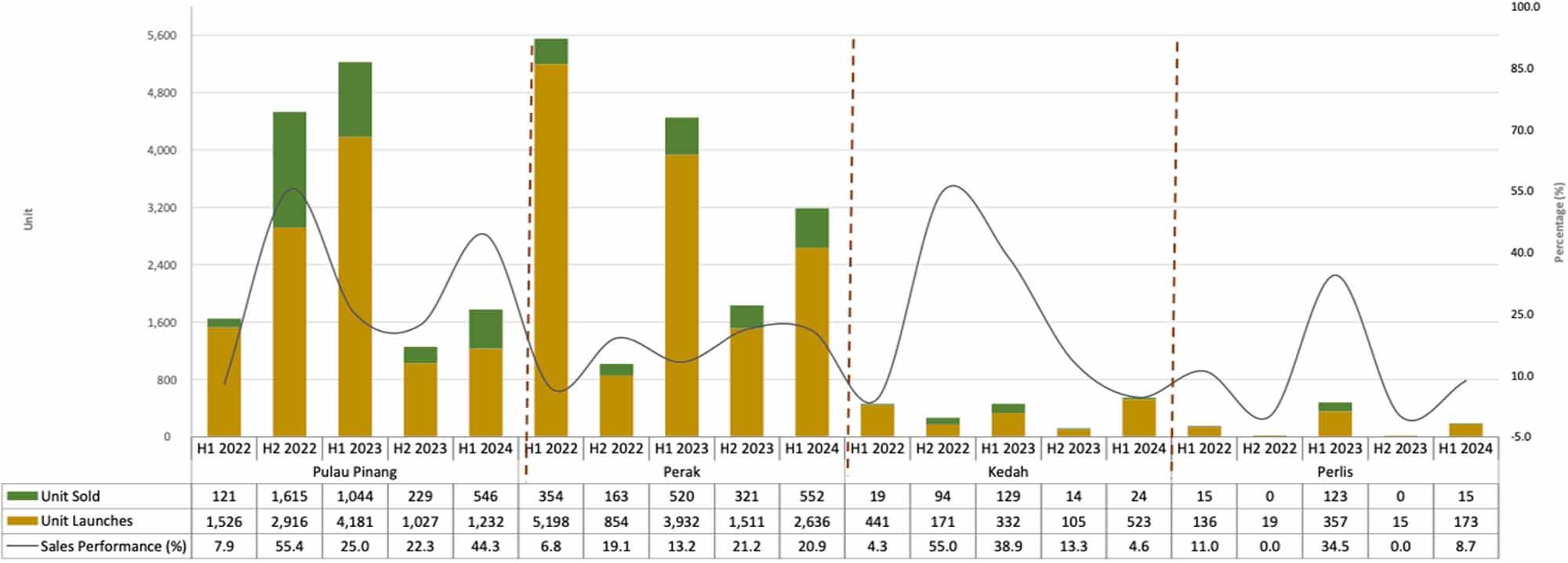

The performance of the primary market in the region is moderate compared to H1 2023. New launches in Kedah increased by 57.5% while Pulau Pinang, Perlis and Perak decreased by 70.5%, 51.5% and 33.0% respectively.

By property type, two to three storey terraced houses formed the bulk of the new launches in Pulau Pinang. Single storey terraced houses make up the majority of new launches in Kedah. Meanwhile in Perlis, single storey semi-detached houses were the main contributors while condominiums / apartments were the main contributors to newly launched units in Perak.

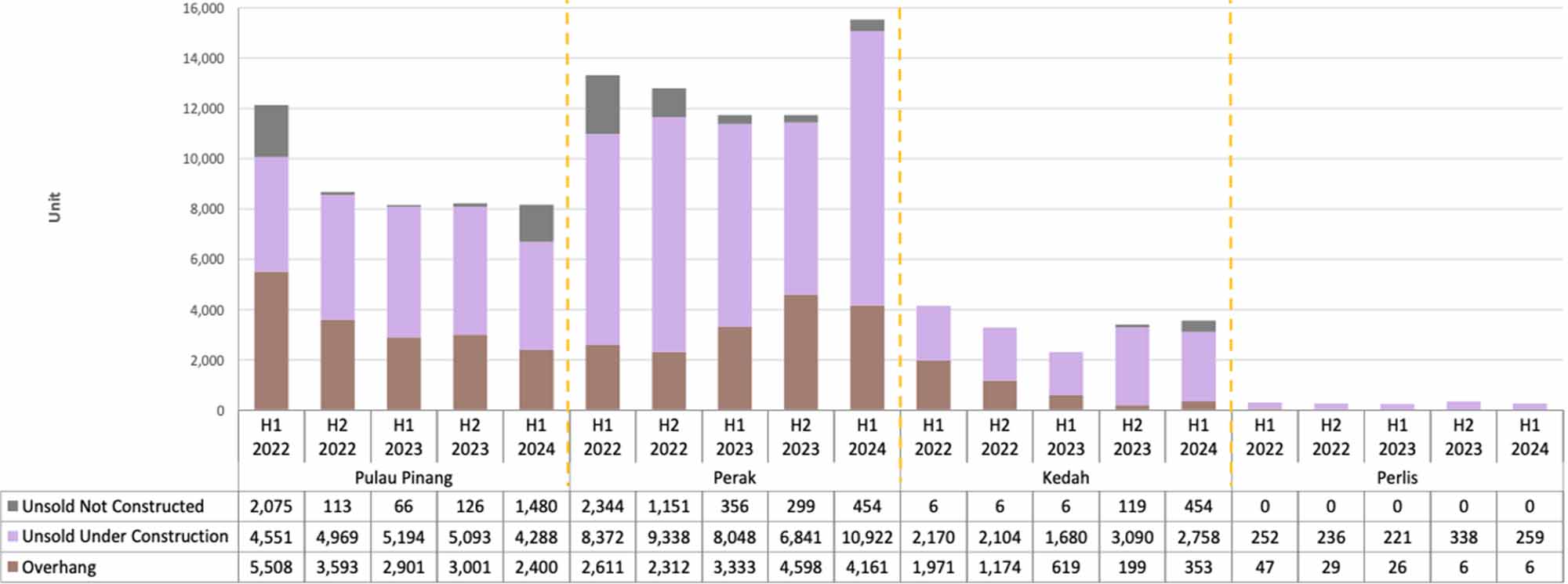

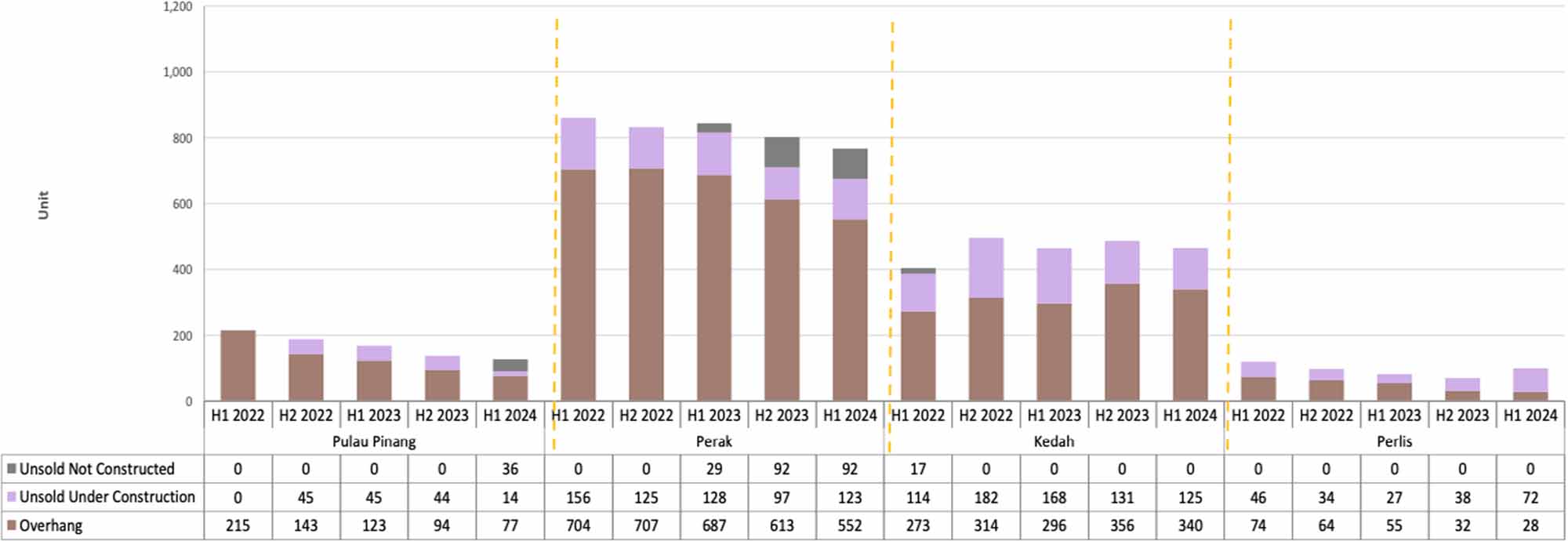

The residential overhang situation remained challenging in the Northen Region. Perak recorded the highest number of residential overhang units in the country, accounting for 18.4% (4,161 units) of the national total. In Kedah, the number and value of overhang continued to increase in the review period. Nevertheless, the overhang performance in Perak and Pulau Pinang showed improved as the overhang units and value contracted. Meanwhile, in Perlis the overgang performance remained unchanged.

Unsold under construction in Perak increased to 10,922 units compared to H2 2023. However, the situation in Perlis, Pulau Pinang, and Kedah eased as unsold unit were reduced by 23.4%, 15.8% and 10.7% respectively. Unsold not constructed situation remains challenging in Pulau Pinang, Perak, and Kedah, as these states recorded a higher number of units compared to H2 2023. There were no unsold units in Perlis.

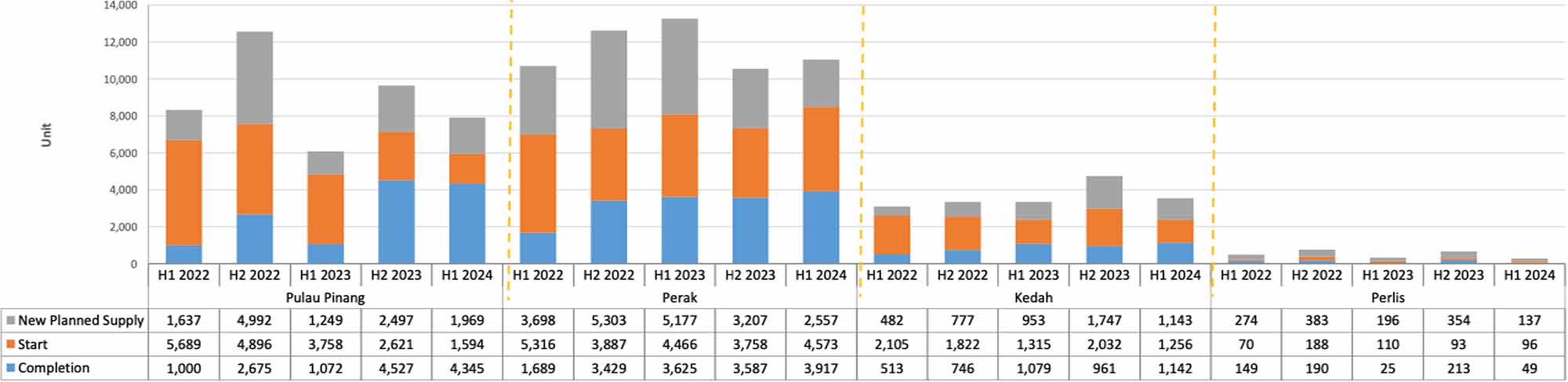

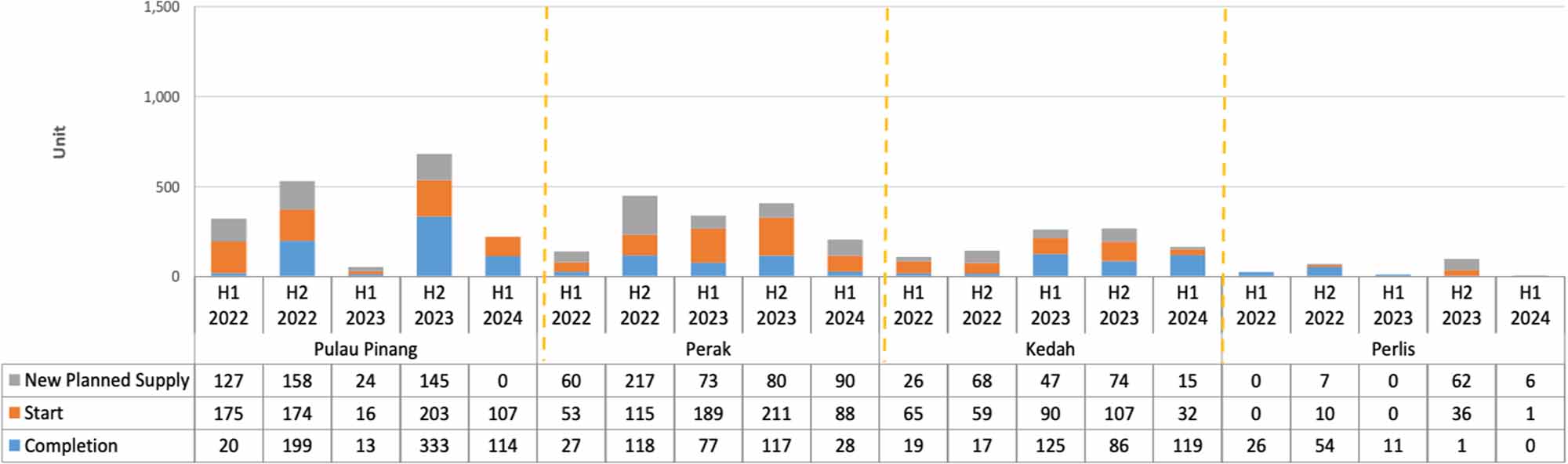

The construction activities varied among the states in the Northern Region. Completed units in all states as compared to H1 2022. Starts in all states decreased except for Perak, which increased by 2.4%. New planned supply for Pulau Pinang and Kedah increased by 57.6% and 19.9%, while Perak and Perlis dropped by 50.6% and 30.1%, respectively.

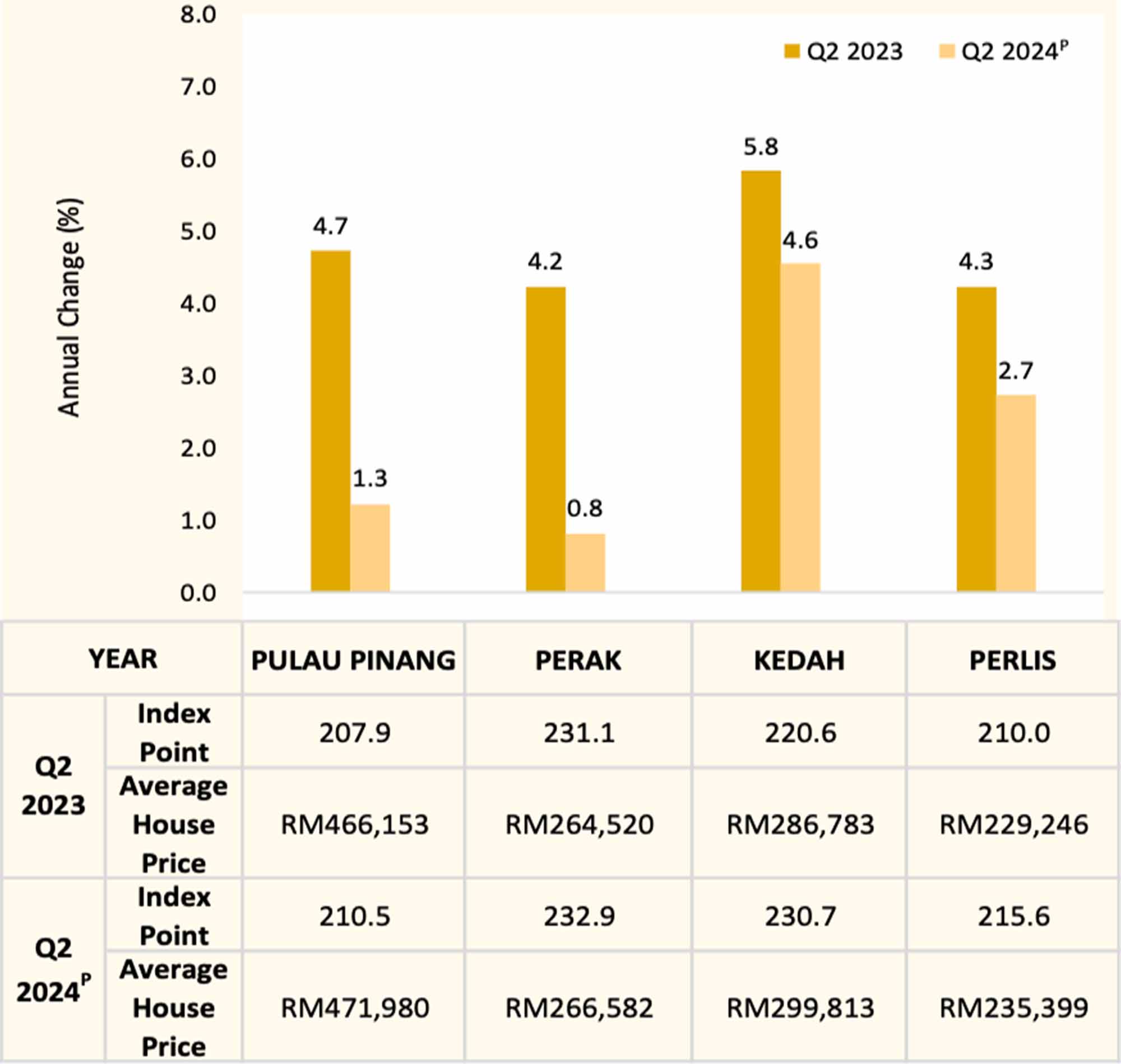

The All House Price Index in the Northern Region shows a positive trend in Q2 2024P . Kedah showed the highest increase of 4.6%, followed by Perlis by 2.7%, Pulau Pinang by 1.3% and Perak by 0.8%. Pulau Pinang recorded the highest average house price at RM471,980, followed by Kedah at RM299,813, Perak at RM266,582, and Perlis at RM235,399.

The all House Index for Kuala Lumpur and Selangor stood at 196.6 points and 220.8 points, respectively. The average all house price for Selangor stood at RM535,390 in Q2 2024P , an increase from RM534,788 in Q2 2023, while Kuala Lumpur stood at RM780,728, a decrease from RM786,956 in Q2 2023.

The residential rental market for landed properties in city areas such as George Town, Alor Setar and Kangar, were generally stable. In Ipoh, the rental increased in the range of 2.3% to 11.1%, depending on the location of the housing schemes. For high-rise rental market, most of the states Ipoh showed a stable rental trend in general, except, for stratified units in several schemes in Pulau Pinang and Perak, which showed a mixed trend.

The commercial sub-sector recorded 3,243 transactions worth RM2.83 billion in the review period. The transaction volume and value decreased by 5.8% and 36.0% as compared to H1 2023.

Transaction value recorded an increase of 43.7% in Kedah, followed by Perlis (40.5%) and Perak (37.3%), while Pulau Pinang dropped by 55.4%.

The shop sub-sector remained a key contributor to the commercial property market in the Northern Region, accounting for 72.2% (2,340 transactions worth RM1.45 billion) of the commercial property transactions (3,243 transactions worth RM2.83 billion). By state, Perak led the market with 43.9% share, followed by Pulau Pinang (27.2%), Kedah (25.3%) and Perlis (3.6%). In terms of transaction value, Pulau Pinang drove the market with 42.0% share, followed Perak (37.9%), Kedah (16.3%) and Perlis (3.8%).

Against H2 2023, the shop overhang in the Northern Region decreased by 11.3%. Correspondingly, the overhang value also decreased in tandem. On the other hand, unsold under construction recorded an increase of 7.7%. No unsold not constructed units were recorded in Kedah and Perlis, except Perak and Pulau Pinang which with 92 units and 36 units, respectively.

The construction activities varied among the states in the Northern Region. The completion in Pulau Pinang increased almost eightfold compared to H1 2023. Contrarily, Perak and Kedah recorded a drop of 63.6% and 4.8%, respectively while there was no completion in Perlis. Starts in Pulau Pinang and Perlis increased except for Kedah and Perak, which decreased by 64.4% and 53.4%, respectively. The new planned supply for in Perak and Perlis also increased, except Kedah, which decreased by 68.1%, while there was no new planned supply in Pulau Pinang.

Prices of shops in all states were generally stable. In Pulau Pinang, pre-war shop transacted at price ranging from RM1,100,000 to RM2,500,000 while in Perak, pre- war shop transacted at price ranging from RM200,000 to RM1,280,000 depends on location and land size.

Similarly, the rental market also stable across the board. In Pulau Pinang, ground floor shop rents were stable except outside city center showing a mixed movement. New shops with modern designs such as the Elevate @ Gravitas and Juru Sentral recorded high rental rates ranging from RM5,000 to RM9,000 per month.

There were 144 transactions worth RM90.33 million of service apartment/SOHO recorded in the Northern Region. The transaction volume increased by 33.6% compared to H1 2023 (217 transactions worth RM118.54 million), while the transaction value decreased by 23.8%.

Against H2 2023, the overhang for serviced apartment / SOHO in Pulau Pinang decreased to 288 units worth RM379.31 million (H2 2023: 346 units worth RM440.01 million). In Perak, the overhang for serviced apartment / SOHO increased to 135 units worth RM65.86 million (H2 2023: 28 units worth RM7.02 million). Compared to Pulau Pinang and Perak, there were no overhang in Kedah and Perlis. Meanwhile, unsold under construction in Pulau Pinang decreased by 10.0% to 1,366 units, while there were no unsold under construction units in Perak, Kedah and Perlis. Unsold not constructed in Pulau Pinang increased significantly by almost twenty seven fold to 934 units, while there were no unsold not constructed units in Perak, Kedah and Perlis.

The new construction activity was mixed in the review period. Pulau Pinang and Perak recorded 588 and 196 units in the new planned supply, respectively. Kedah and Perlis did not record any new activity.

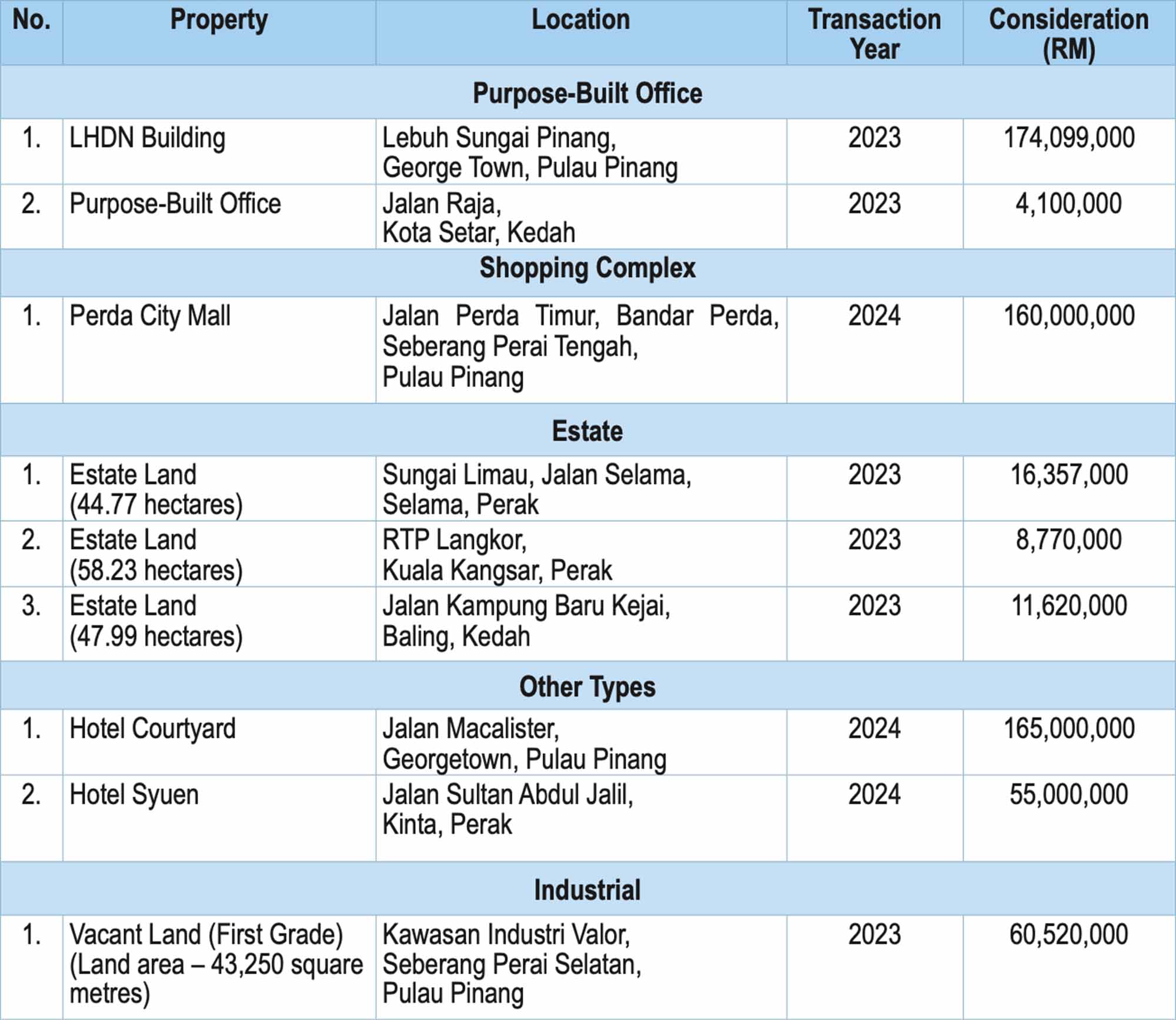

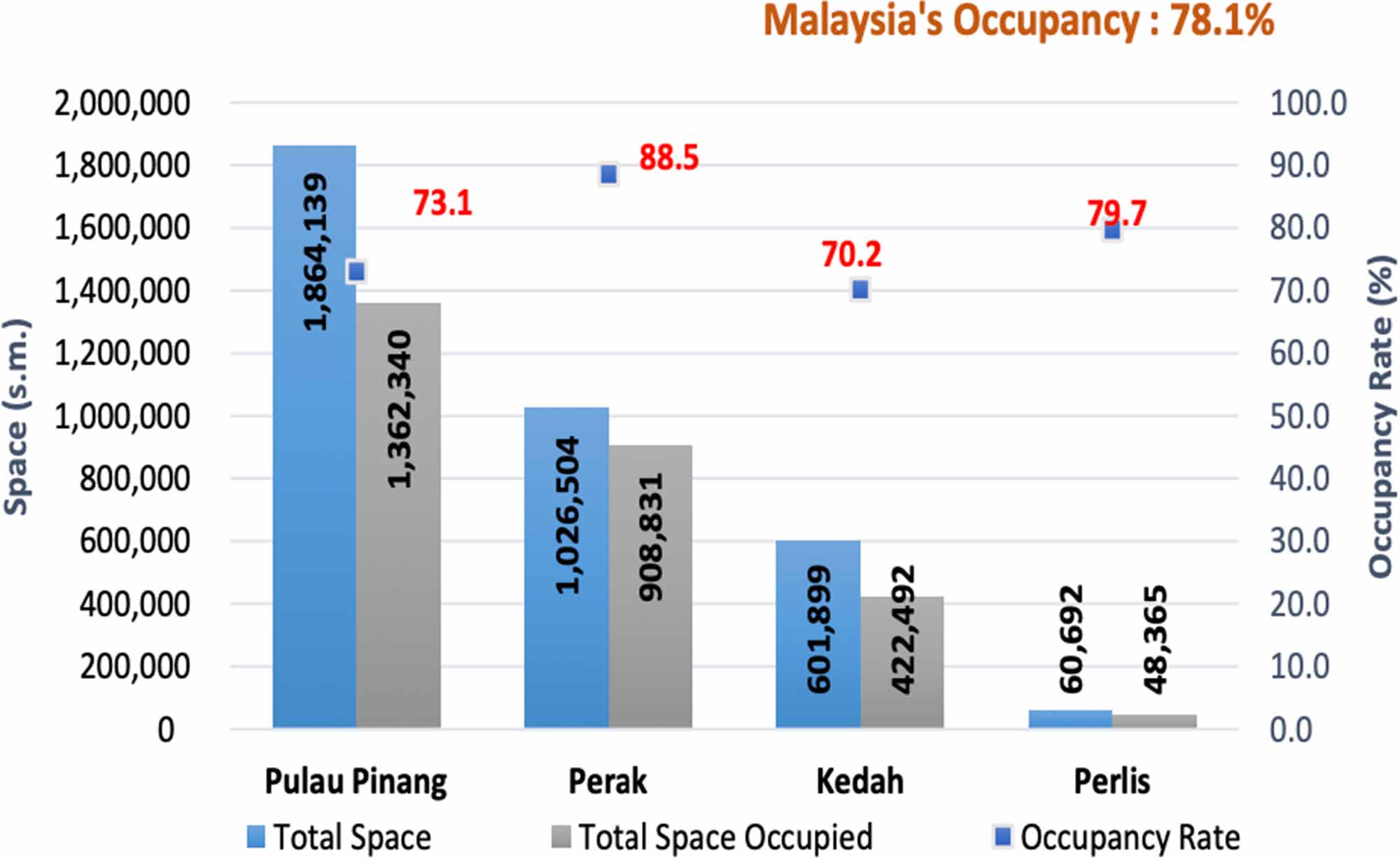

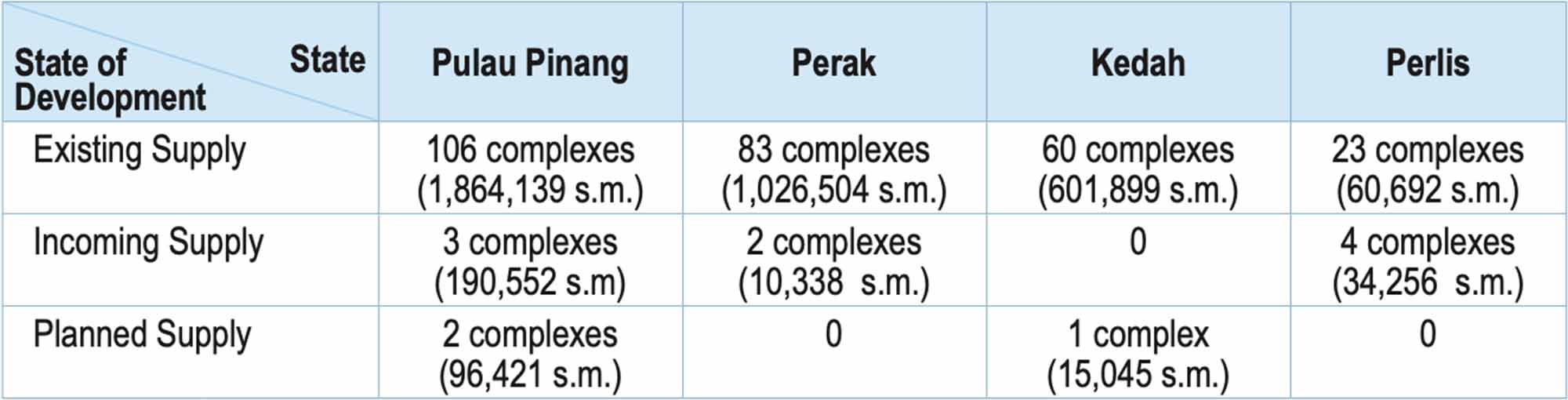

The review period recorded one transaction of shopping complex in the Northern Region, namely Perda City Mall in Bandar Perda, Seberang Perai Tengah, Pulau Pinang.

The overall occupancy rate for shopping complexes in the Northern Region recorded 77.2%, a growth of 0.6% compared to H1 2023. By state, Perak experienced an increase in occupancy rate of 1.5%, followed by Kedah by 0.4% and Pulau Pinang by 0.2%, while Perlis experienced a drop of 4.8%.

One new completion was recorded in the Northern Region during the review period, namely Econsave Temasek in Ipoh, Perak.

Rental movement in retail space showed mixed performance depending on the types and locations of the property. In Pulau Pinang, Lotus’s Bukit Mertajam recorded a growth in rental ranging 13.0% to 26.7% and in Perak, Mydin Mall recorded a growth in rental ranging 2.1% to 11.9%. In Kedah and Perlis, the rental rates remained the same for most of the retail space.

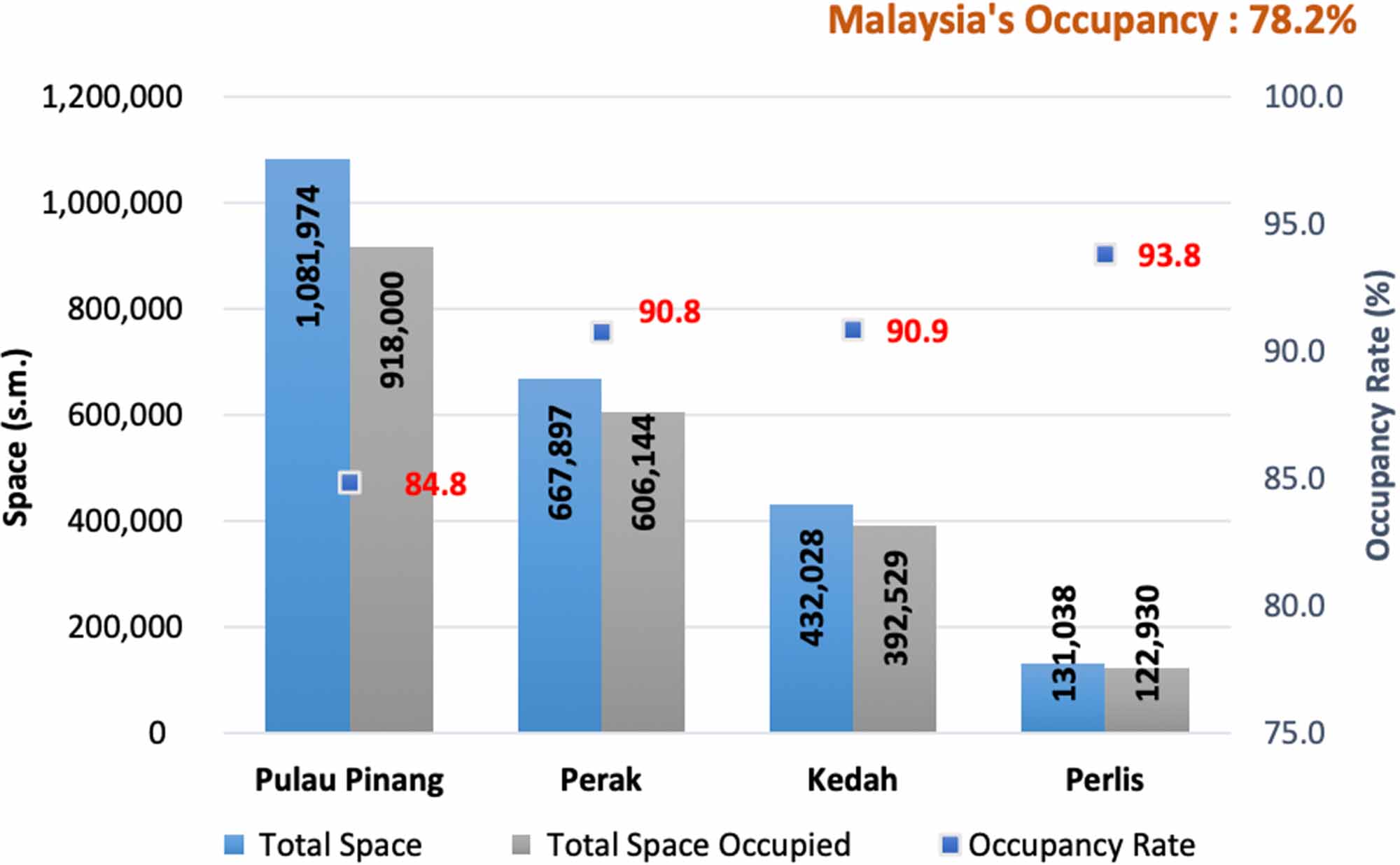

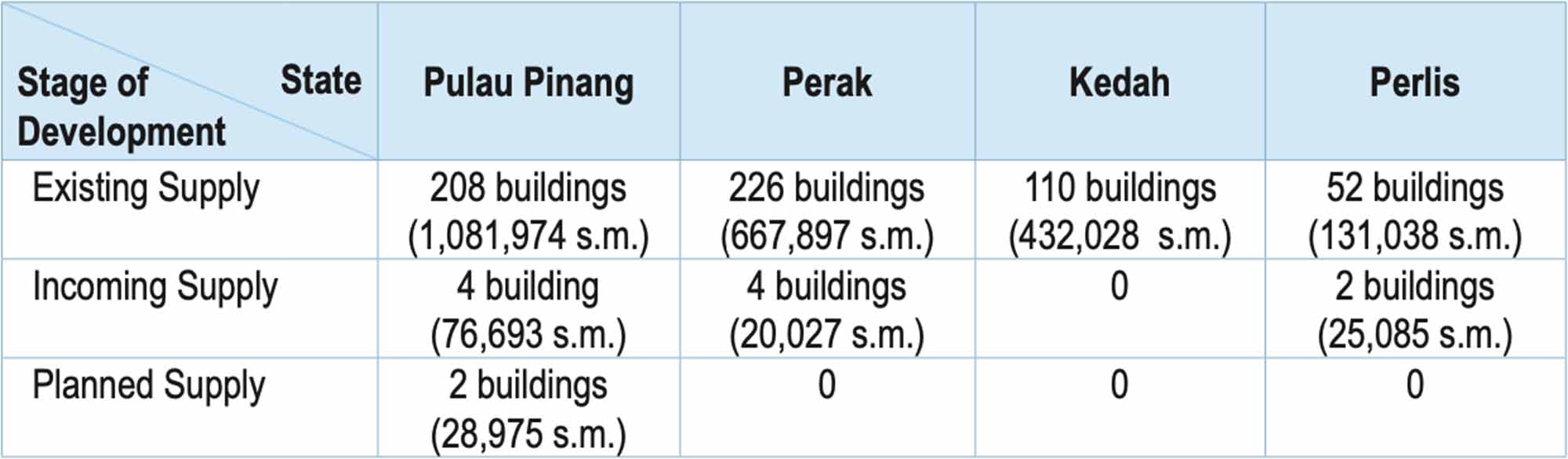

The review period recorded two transactions of purpose-built office in the Northern Region, namely LHDN Building in George Town, Pulau Pinang and a Purpose-Built Office in Bandar Kota Setar, Kedah.

The purpose-built office segment showed mixed performance within the review period. The overall occupancy rate in Kedah increased by 0.6%, followed by Perlis by 0.3%, while other states showed downward trend, led by Perak (1.6%), followed by Pulau Pinang (1.4%).

The new construction activity was less active. There was no completion during the review period.

Rentals of purpose-built offices were largely stable across the board, with a few exceptions. In Perak, rental increments were captured at Lembaga Tabung Haji Building (10.2%), Menara Taiko (6.9%), Plaza Teh Teng Seng (6.8%-6.9%), Menara SSM Perak (5.6%) and KWSP Building (4.9%-5.4%). Hunza Tower Gurney Paragon recorded the highest rental in the Northern Region at RM56.03 p.s.m.

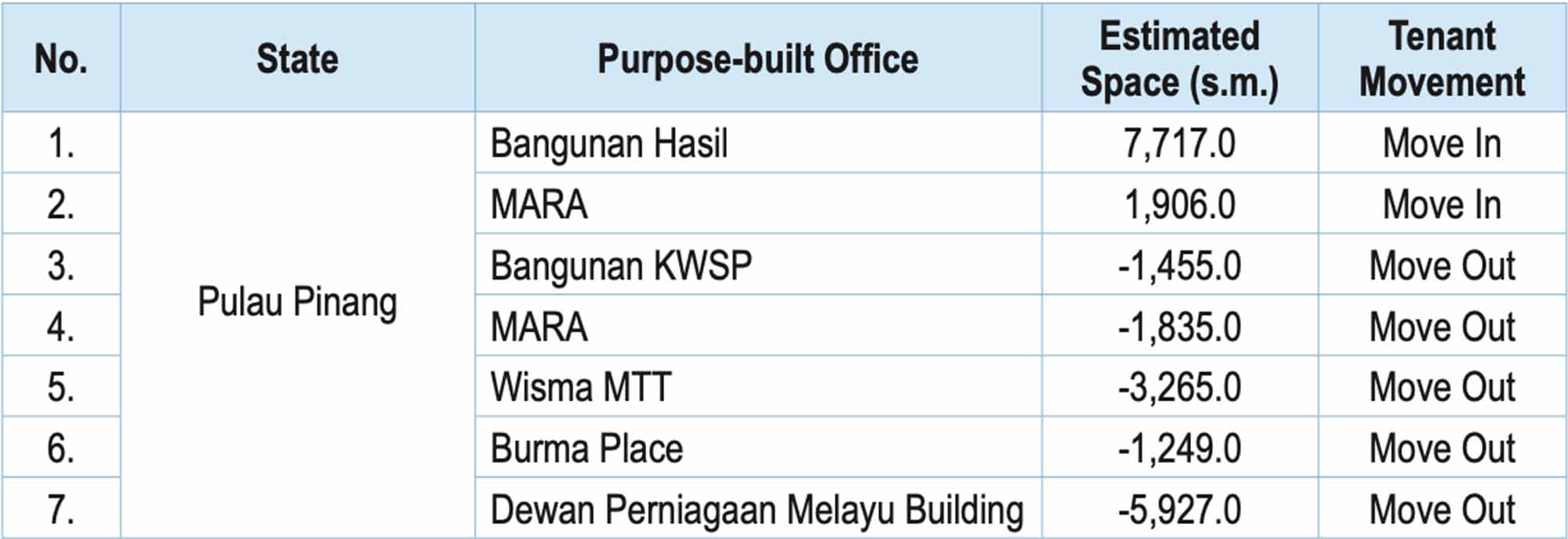

Table below showed the list of some pertinent tenant movements recorded in Pulau Pinang.

The review period saw five transactions in the Northern Region, which are Hotel Fuhow in Bandar Butterworth, Seberang Perai Utara, Pulau Pinang, Hotel Courtyard in Georgetown, Pulau Pinang, Hotel Syuen in Kinta, Perak, 88 Resort Villa Riadah in Manjung, Perak, and a chalet in Bandar Kuah, Langkawi.

In the leisure sub-sector, the Northern Region recorded one hotel under new planned supply in Perak during the review period. The hotel offers 303 rooms in total once completed.

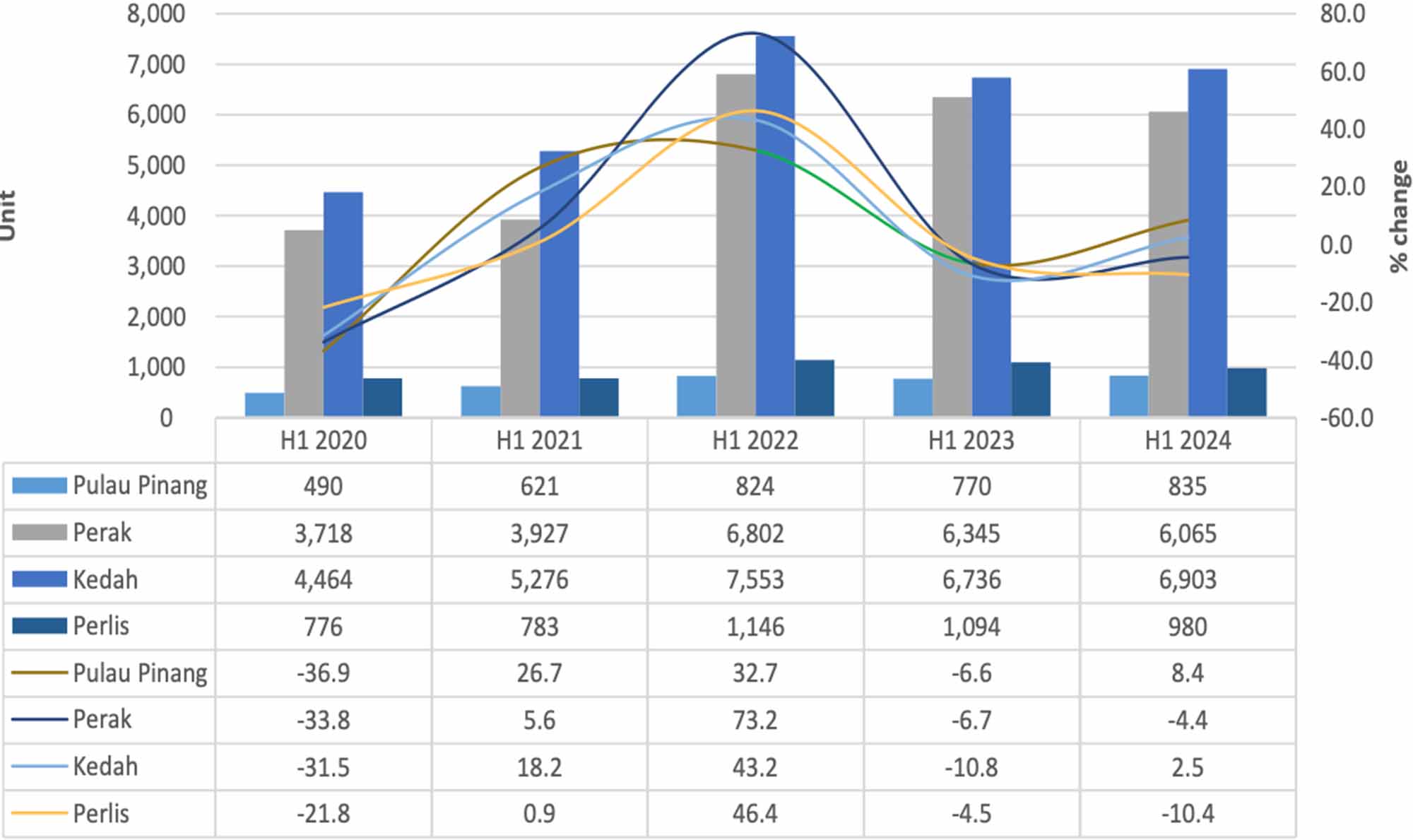

The agriculture sub-sector remains the second leading sub-sector after residential, with 14,783 transactions, accounting for 28.7% of the region’s property transactions. Kedah was the main contributor to agriculture market activity with 6,903 transactions, followed by Perak with 6,065 transactions, Perlis with 980 transactions, and Pulau Pinang with 835 transactions.

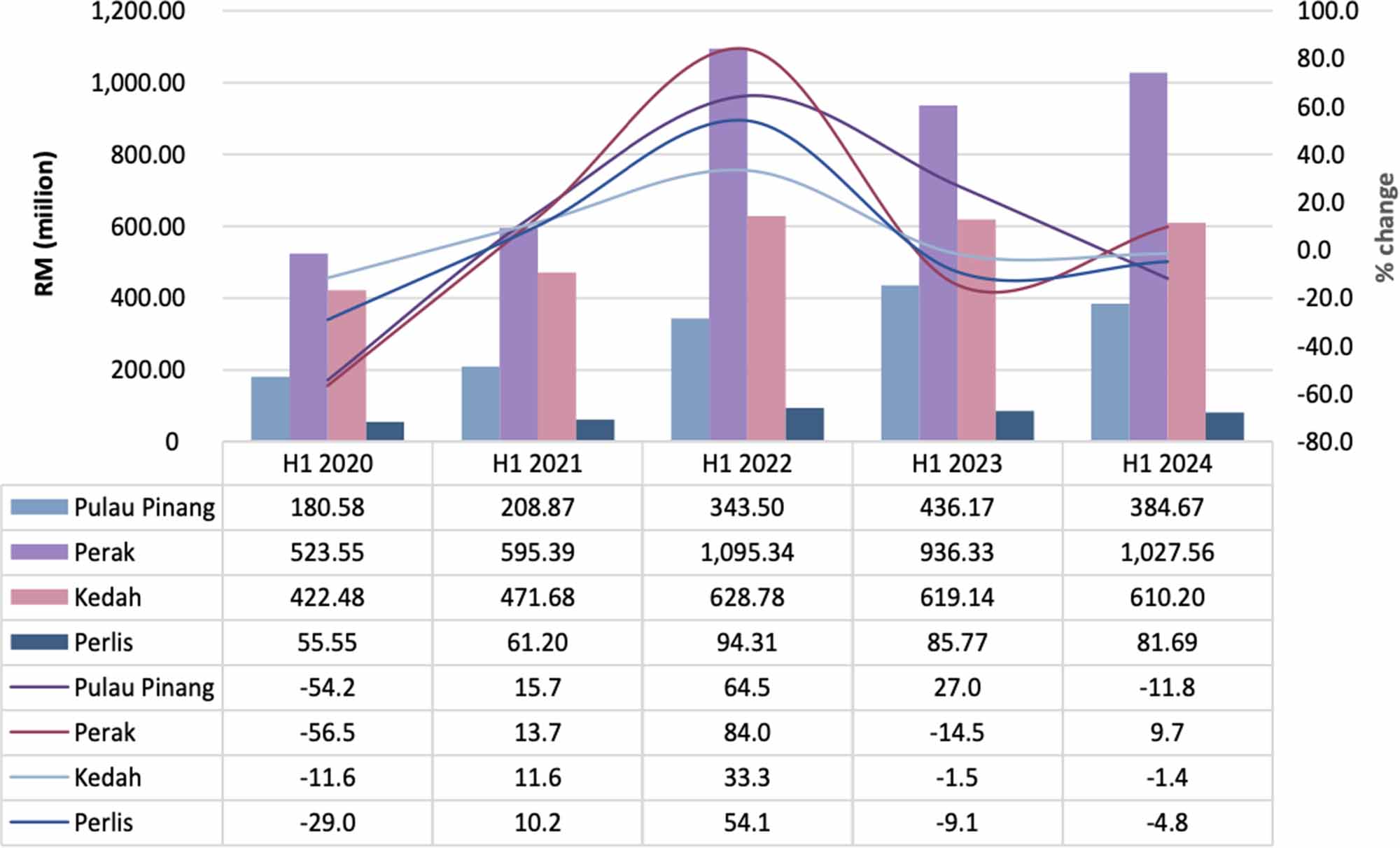

The agriculture sub-sector recorded RM2.10 billion transactions value equivalent to 12.5% of total transactions value in the region. All the states recorded a drop of value led by Pulau Pinang (11.8%), Perlis (4.8%) and Kedah (1.4%), while Perak recorded an increase of 9.7%.

Prices of agriculture property were stable overall, with marginal price movements recorded in certain areas. In Perlis, paddy class 1 remained active, with price appreciation recorded in the range of 3.0% to 19.5% compared to H2 2023. Oil palm and rubber land’s transaction was active in Perak and recorded mixed price movement depending on the location of the land. Orchard, rubber, oil palm and paddy land’s transactions was active in Kedah and recorded stable price movement.

| No. | Infrastructure | Descriptions | Current Development Status |

|---|---|---|---|

| 1. | Bayan Lepas Light Rail Transit (BLLRT) |

|

Proposal Stage |

| 2. | Tun Dr Lim Chong Eu Expressway - Air Itam Bypass (Package 2) |

|

Under construction and expected to be completed in Q1 2025 |

| 3. | Penang South Reclamation (PSR) Project – Silicon Island |

|

Under construction |

| 4. | Penang Technology Park |

|

Proposed Development |

| 5. | Lumut Maritime Terminal (LMT 2) |

|

Under Construction and expected to be completed by 2026 |

| 6. | Taiping Solar PV Park II |

|

Under construction and expected to be completed by 2025. |

| 7. | By Pass from Pelubang Water Treatment Plant (Piping) |

|

Under construction and expected to be completed by 2024 |

| 8. | Bukit Selambau Water Treatment Plant Upgrading Project |

|

Under construction |

| 9. | Darulaman Lagenda |

|

Under construction |

| 10. | Perlis Inland Port – Bonded Road (CVIA) |

|

Under construction Project status: 15% completed. |

| 11. | Kangar Sentral |

|

Under construction |

| 12. | Sanglang Integrated Jetty |

|

Proposal Stage |

| No. | Development | Descriptions | Current Development Status |

|---|---|---|---|

| 1. | Andaman Island |

|

Under construction |

| 2. | Setia Fontaines Township |

|

Under construction |

| 3. | The Light Waterfront Penang |

|

Under construction |

| 4. | Eco Horizon |

|

Under construction |

| 5. | Automative High Technology Valley (AHTV) |

|

Proposal Stage |

| 6. | Automative High Technology Valley (AHTV) Township |

|

Proposal Stage |

| 7. | Ipoh Raya Integrated Park |

|

Phase 1 is expected to be completed by 2028 and the whole project is expected to be completed by 2043. |

| 8. | Langkawi Premium Outlet |

|

Phase 1 Completed Other Phase Expected to be completed by 2026 |

| 9. | Hospital Sultanah Maliha, Langkawi |

|

Under construction and expected to be completed in Q2 2025. Project status: 26% completed |

| 10. | Sekolah Menengah Kebangsaan Bohor Jaya |

|

Under construction and expected to be completed in Q1 2025. Project status: 40% completed |

| 11. | Pusat Kanser Wilayah Utara |

|

Expected to be completed in Q2 2025 |

| 12. | Chuping Valley Industrial Area (CVIA) |

|

Under construction |

| 13. | Pavilion Padang Besar |

|

Under construction |

| 14. | Chuping Agro Valley – Integrated Dairy Farm |

|

Proposal Stage |

| 15. | Plazaria Padang Besar |

|

Under construction |

| 16. | Kangar Jaya Mall (C-Mart 3) |

|

Under construction Project status: 55% completion. |

| No. | State | Descriptions |

|---|---|---|

| 1. | Perak |

The issuance of Garis Panduan Piawaian Perumahan Negeri Perak guideline.

This guideline is issued again after it was issued in 2019. The guideline acts as a reference for the Local Authorities and technical agencies of the State of Perak to plan and control the development of all types of housing. In addition, it is easier for developers to design layouts and provide public facilities and infrastructure. |

| 2. | Kedah |

Major Development driven by high impact project

(a) Koridor Bandar Sempadan, in the district of Kubang Pasu and Padang Terap (b) Kedah Aerotropolis, in the district of Kuala Muda (c) Bandar Teknologi, in the district of Kulim (d) Pembangunan Tenaga dan Pelabuhan, in the district of Yan. |

| 3. | Perlis |

1) Perlis Land Rules 1987

- Amendment of the Perlis Land Rules 1987 is in the process of revising rates and service fees in Perlis. 2) Perlis State Property Development Policy (2024 Amendment) - Among the essences of the Perlis State Real Estate Development Policy are as follows:- a) The selling price of affordable houses (landed) is between RM80,000.00 to RM180,000.00 b) The sale price of affordable houses (strata) is between RM80,000.00 to RM150,000.00 c) Construction of affordable houseing is 30% of the total land area developed or levy payment (affordable housing replacement money) of RM75,000.00 per unit. d) The selling price of affordable shops is below RM200,000.00 per unit (20% of the number of shop units built). |

National Real Estate Award Firm of the Year 2021, 2022, 2023, 2024

National Real Estate Award Industrial Firm of the Year 2020, 2022, 2023

National Real Estate Award Technology Firm of the Year 2021

National Real Estate Award Real Estate Agent of the Year 2020

National Real Estate Award Specialised Project of the Year 2019

National Real Estate Award CEO

National Real Estate Award Commercial Agency

National Real Estate Award Million Dollar Roof Top

National Real Estate Award Top Realtor

Star Property Best Practice Award 2019

Star Property All-Star Agency 2017

iProperty Elite Project Marketing Agency

iProperty Agency of the Year (Platinum)

Asia Pacific Property Awards

Asia Pacific Residential Property Awards